Owning a seasonal camp in Central New York brings unique challenges that year-round homeowners rarely face. Extended periods away from your property create vulnerabilities that standard insurance approaches often don't address adequately. When problems arise—from frozen pipes to trespasser incidents—you need coverage designed for these specific risks.

At the Horan insurance agency, we work with carriers who understand seasonal property exposures throughout Central New York. Our experience with camps and seasonal homes helps us identify coverage gaps that could leave you facing unexpected costs.

This article explores three critical coverage types that can help address the unique risks seasonal camps face, and why understanding these options matters for helping to secure your investment.

Understanding Why Camps Need More Insurance Coverage Than Regular Homes

Camps are more vulnerable to disasters than regular homes. Why? Because they’re often left unattended for long periods of time. A small problem can quickly escalate into a major crisis without anyone noticing or intervening.

- A pipe can burst and flood the entire camp

- A fire can spread and destroy the property, or

- A trespasser can injure themselves and sue you for negligence.

That’s why you need to have adequate insurance coverage for your camp. You don’t want to risk losing your precious investment or facing a costly lawsuit. There are many types of coverages that can help address your camp's risks, but these three are among the most important ones. Consider these recommended coverages.

Critical Camp Coverage 1: Replacement Cost Value

Understanding the first coverage requires examining how your policy values both your structure and personal belongings.

Apply This to Both the House and Contents

Your camp insurance policy may not work the same way as your homeowners policy for your primary home. You need to make sure that your policy covers the full cost of rebuilding your camp if it’s destroyed by a covered peril.

Some insurers may only offer actual cash value coverage (ACV), which means they’ll deduct depreciation from your payout. This could leave you with a big gap between what you receive and what you need to rebuild.

To help address this, you should look for a policy that offers replacement cost value coverage (RCV) for your dwelling. This type of coverage will pay for the current cost of labor and materials to rebuild your camp, regardless of depreciation.

For example, imagine your camp sits on the edge of Lewis County, with access to a choice ATV and snowmobile trail system—ideal because you have a decent snowmobile policy in place.

But you bought a camp insurance policy that only offers actual cash value coverage for your dwelling. You thought you were saving money by choosing a cheaper policy and didn’t consider the impact of depreciation on your payout.

One day, a severe storm hits your area and causes a tree to fall on your camp. The roof collapses, and the interior is damaged by water and debris. You’re thankful that no one was hurt, but you’re worried about the extent of the damage.

When you call your insurance company to file a claim, hoping to get enough money to rebuild your camp, you’re disappointed by their offer. They tell you that they will only pay for the depreciated value of your camp, which is much lower than the current cost of rebuilding it.

You realize you have to pay the difference out of pocket, which could be tens of thousands of dollars. If only you’d chosen a policy that offers replacement cost value coverage for your dwelling that would have paid for the full cost of rebuilding your camp, despite depreciation.

The same principle applies to your personal belongings inside the camp. If you have valuable items such as furniture, electronics, appliances, or clothing, you don’t want to settle for actual cash value coverage. This could result in a low payout that won’t cover the cost of replacing your items with new ones.

Instead, you should opt for replacement cost coverage for your personal property. This type of insurance will compensate you for the full expense of purchasing new items of comparable quality and type.

Replacement cost coverage may cost more than actual cash value coverage in terms of premiums, but it can save you a lot of money and hassle in the event of a claim. It can also help you preserve your investment and legacy for future generations.

Most insurers have a minimum requirement for replacement cost coverage, which is usually 80% of your home’s replacement value. If you fall short of this requirement, your insurer may only pay a portion of the replacement costs.

Therefore, it is important to review your policy regularly and update it as needed to reflect the current value of your camp and belongings.

Critical Camp Coverage 2: Special Form

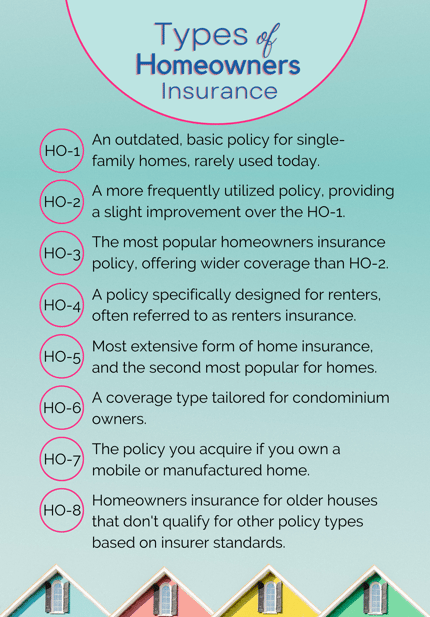

One of the most important things to look for when buying camp insurance is the type of policy form you’re getting. Some policies may have exclusions or limitations that could leave you exposed to certain risks that are common for seasonal homes. That’s why you should consider a policy that offers Special Form coverage, also known as HO-3 or HO-5.

One of the most important things to look for when buying camp insurance is the type of policy form you’re getting. Some policies may have exclusions or limitations that could leave you exposed to certain risks that are common for seasonal homes. That’s why you should consider a policy that offers Special Form coverage, also known as HO-3 or HO-5.

While this may sound like insurance jargon, we'll explain it simply.

Special Form coverage means that your policy covers your dwelling and other structures on an open perils basis. This means that your policy will cover any damage or loss to your camp unless it is specifically excluded in the policy.

This is different from other policies that only cover your camp for a list of named perils, such as fire, lightning, windstorm, etc. If your camp suffers damage from a peril that isn’t on the list, you won’t be covered. It’s that straightforward.

Some of the perils that may not be covered by other policies but are covered by Special Form policies include:

- Water damage (including from ice and snow)

- Vandalism

- Burglary

- Theft

- Power failure

- Falling objects

- Weight of ice, snow, or sleet

- Accidental discharge or overflow of water or steam

- Sudden and accidental tearing apart, cracking, burning, or bulging of a built-in appliance like a water heater or centralized air conditioner or heating system

These perils could affect your camp and cost you a lot of money if you don’t have adequate coverage.

Let’s say you have a cozy camp way up in North Country—in Colton, New York—and buy a seasonal home insurance policy that only covers your dwelling and other structures for a list of named perils, such as fire, lightning, windstorm, and so forth.

You thought you were getting a good deal at the time and didn’t pay attention to the exclusions or limitations of your policy.

One night, while you’re away from your camp, seasoned burglars break in and clean out your valuables—including expensive fishing gear, hunting rifles, and more. They also vandalize your walls and furniture with graffiti and damage your appliances. The vandals leave a mess of water and steam from the overflowing sink and the broken water heater.

When you return to your camp, you’re devastated by the scene. You call your insurance company to file a claim, hoping to get some compensation for your losses. But you’re in for a rude awakening.

Your agent says your policy doesn’t cover burglary, vandalism, theft, or water damage. These are some of the perils that are covered by Special Form policies but not by named peril policies. You’re left with no coverage and have to pay for the repairs and replacements out of your own pocket.

In cases like this, Special Form coverage can be worth the extra cost because it covers any damage or loss to your camp unless it is specifically excluded in the policy.

The difference between HO-3 and HO-5 policies is that HO-3 policies only cover your personal property (such as furniture, electronics, clothing, etc.) on a named perils basis, while HO-5 policies cover your personal property on an open perils basis as well.

HO-5 policies offer higher coverage limits and replacement cost coverage for personal property. Replacement cost coverage means that your policy will pay for the full cost of buying new items of similar quality and kind without deducting depreciation.

HO-5 policies are more comprehensive and expensive than HO-3 policies, but they offer more coverage and greater confidence for your camp and belongings. Depending on the value and condition of your camp and personal property, you may want to consider getting an HO-5 policy instead of an HO-3 policy.

Critical Camp Coverage 3: Liability

The third critical coverage area focuses on liability exposures that seasonal property owners often underestimate.

Consider Higher Liability Limits on Your Camp

Rural seasonal camps allow you and your family to enjoy the natural beauty and tranquility of the countryside. But owning a seasonal camp also comes with some risks and responsibilities. One of them is the possibility of trespassers on your property.

Since you’re not always present to monitor your camp, you may not know who is passing through or staying on your land. Some trespassers may be harmless, such as hikers, hunters, or neighbors, but others may be malicious, like vandals, thieves, or squatters.

If any of them get injured or cause damage on your property, you may be held legally liable for their medical bills, repairs, or lawsuits. This is true even if you’ve posted signs that say “No trespassing” or “Private property” on your land.

That’s why it’s essential to have adequate liability insurance for your rural seasonal camp. Liability insurance covers the costs of legal fees and settlements if someone sues you for an injury or damage that occurred on your property.

It also helps address claims that arise from your own actions or negligence, such as accidentally starting a fire or injuring someone with your vehicle. Liability insurance can help you address significant financial consequences and legal troubles in case of an unexpected incident.

The amount of liability insurance you need depends on several factors, such as the size and location of your property, the frequency and duration of your visits, the activities you do on your land, and the potential hazards that exist on your property.

You should consult with an insurance agent who has experience with rural properties to explore coverage options and learn about potential considerations based on your situation. Consider purchasing as much liability insurance as the carrier will offer you because the costs of lawsuits can be very high and unpredictable.

Rural seasonal homes can be a great source of enjoyment and relaxation for you and your family. But they also require careful planning and coverage considerations to help address legal problems and financial losses. By investing in suitable liability insurance coverage, you can have greater confidence and enjoy your rural retreat with less concern about trespassers.

Explore Adequate Coverage for Your Cherished Retreat

Now that you're aware of these important coverages you may want to consider for your rural camp, it's time to take action. Don't let a random accident damage your cherished rural retreat. Whether it's a fire, a storm, a theft, or a lawsuit, you need to be prepared for the unexpected. Your seasonal camp is more than just a property---it's a legacy.

That's why you want an insurance policy that addresses these key areas.

You've worked hard and probably searched extensively to secure this special property. We know your camp is a special place for you and your family. That's why we want to help you explore coverage options with suitable insurance coverage.

If you're ready to learn about seasonal camp coverage that could benefit your family, click the Get a Quote button below to get started. We'll reach out to you and ask some questions about your camp and how you use it. Based on your answers, we'll work with you to explore coverage options that address the specific risks and challenges camps and seasonal properties face.

We have the experience and knowledge to guide you through the process and help you make informed decisions about your insurance coverage. Start enjoying your camp without worrying about the what-ifs.

Let us help you explore insurance options so you can focus on making memories with your loved ones.

If you still need time to decide and would like to expand your knowledge on seasonal camp insurance, read “Navigating Insurance Challenges for Your CNY Camp: Tips and Insights for Helping to Address Your Dream Retreat.”

Topics:

{kind=link}