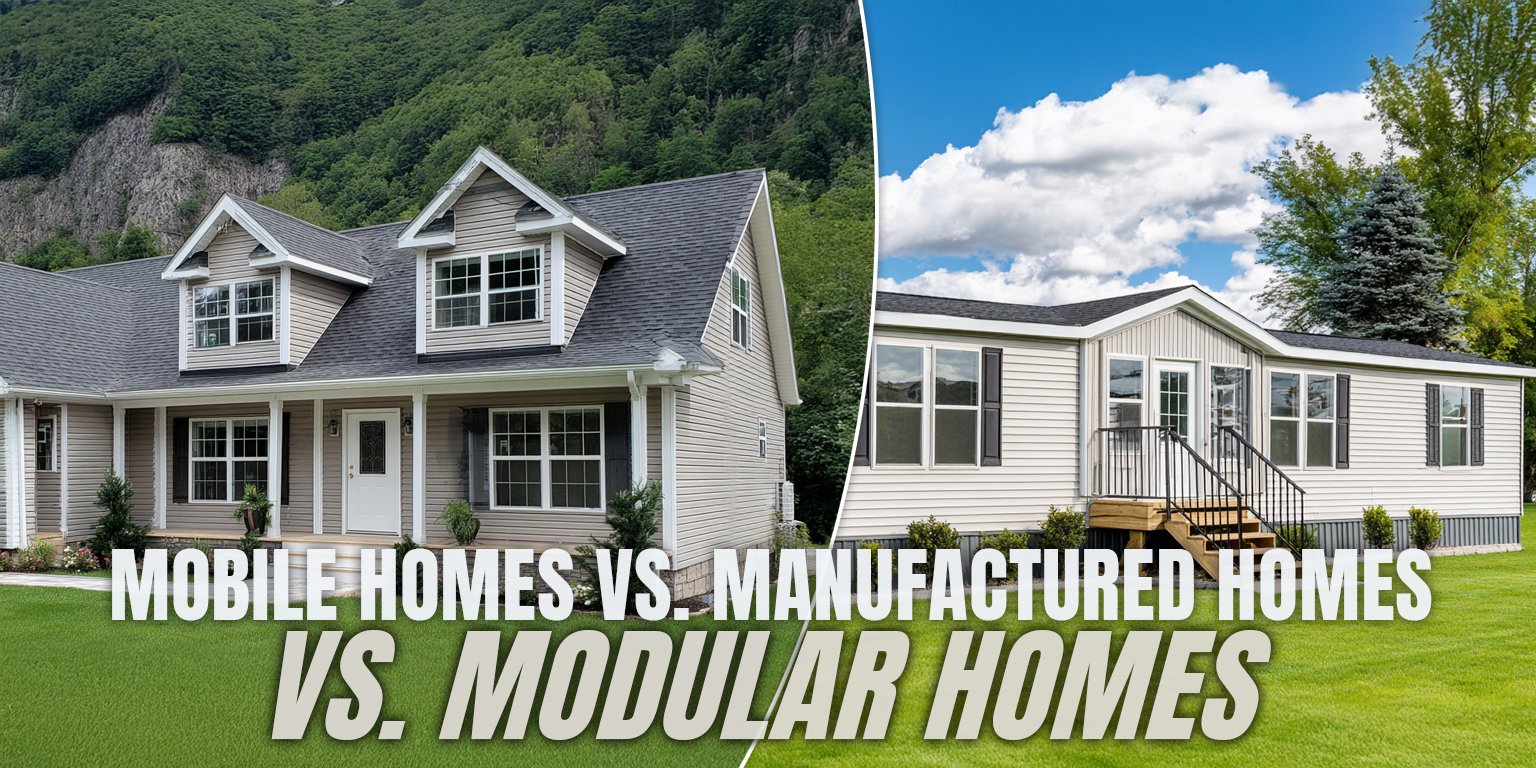

When you're shopping for factory-built housing in Central New York, the terminology can create confusion that affects your insurance decisions. You might hear "mobile home," "manufactured home," and "modular home" used interchangeably, but these terms represent different types of construction with distinct insurance requirements.

Using the wrong term when seeking coverage could lead to delays or inappropriate policy recommendations.

At the Horan insurance agency, we help Central New York residents understand these housing distinctions so they can secure appropriate insurance coverage. We work with carriers who handle different types of factory-built housing to help you explore coverage that matches your home's actual construction and legal classification.

In this article, we'll clarify the differences between mobile homes, manufactured homes, and modular homes, explain how these distinctions affect your insurance options in Central New York, and help you identify which category your home falls into.

Mobile Homes: The Original Factory-Built Housing

Mobile homes represent the earliest generation of factory-built housing, constructed before June 15, 1976, when federal building standards changed. These homes were built without the comprehensive safety and construction standards that govern today's factory-built housing.

In Central New York, you'll find mobile homes primarily in established communities that have been operating for decades. Many of these homes were designed with actual mobility in mind, featuring lighter construction and simpler foundations that made moving feasible, though most haven't moved from their original sites.

Mobile homes typically measure 8 to 12 feet wide and up to 60 feet long. Their construction focused on affordability and basic shelter rather than the durability standards applied to later manufactured homes. This affects both their insurability and replacement costs.

Insurance companies often treat mobile homes differently due to their age and construction standards. Many carriers have restrictions on homes built before 1976, and some won't provide new policies for these older units.

When coverage is available, it typically costs more than comparable manufactured home insurance due to the increased risk factors.

Manufactured Homes: Modern Factory-Built Standards

Manufactured Homes: Modern Factory-Built Standards

The term "manufactured home" applies to factory-built homes constructed after June 15, 1976, when the federal Manufactured Home Construction and Safety Standards (HUD Code) took effect under 24 CFR Part 3280. This date represents a significant shift in quality, safety, and durability requirements.

Manufactured homes built under HUD standards include safety features like smoke detectors, proper electrical systems, and structural elements designed to withstand transportation and setup. These homes display a HUD certification label that proves compliance with federal standards.

In Central New York, most manufactured homes range from 14 to 28 feet wide and can exceed 70 feet in length. Double-wide and even triple-wide configurations provide substantial living space comparable to traditional site-built homes.

Insurance companies generally prefer manufactured homes over mobile homes due to their improved construction standards and safety features. The HUD certification affects financing and placement options, as many manufactured home communities and local jurisdictions require HUD compliance for new installations.

Modular Homes: Site-Built Quality from Factory Construction

Modular homes represent a different category entirely, built to local building codes rather than HUD standards. These homes are constructed in factory sections, transported to building sites, and assembled on permanent foundations that typically include full basements or crawl spaces.

Unlike manufactured homes, modular homes are built to local building codes—the same standards that govern traditional stick-built construction. In Central New York, this means compliance with the New York State Uniform Fire Prevention and Building Code (Uniform Code) under 19 NYCRR Parts 1240-1250 and local municipal requirements.

The construction process involves multiple factory-built sections that are joined together on-site to create what appears to be a traditional home. Once assembled and finished, modular homes are virtually indistinguishable from site-built homes and are often appraised at similar values.

For insurance purposes, modular homes qualify for standard homeowners policies rather than manufactured home coverage. The key difference lies in the foundation and building code compliance—modular homes sit on permanent foundations and meet the same structural requirements as any site-built home in their location.

How These Distinctions Affect Your Insurance Options in Central New York

The classification of your factory-built home directly impacts your insurance options, costs, and coverage availability in Central New York.

- Mobile homes face the most restrictive insurance market. Many carriers won't write new policies for homes built before 1976, and those that do often require inspections and charge higher premiums.

- Manufactured homes have more insurance options available. Several carriers offer coverage specifically designed for homes meeting HUD standards, though age restrictions may still apply with some companies.

- Modular homes receive the same insurance treatment as site-built homes. They qualify for standard homeowners policies from carriers serving Central New York, often at rates comparable to traditional construction.

The foundation type also influences your options regardless of construction method. A manufactured home on a permanent foundation might qualify for standard homeowners coverage with certain carriers, while the same home on piers would require specialized coverage.

Identifying Which Category Your Home Falls Into

Determining your home's classification requires examining specific construction details and documentation.

Check for a HUD certification label, usually located on the exterior of the home near the electrical panel or on an interior wall. This red label indicates a manufactured home built after June 15, 1976. The absence of this label on a factory-built home suggests either a mobile home (pre-1976) or a modular home.

Check for a HUD certification label, usually located on the exterior of the home near the electrical panel or on an interior wall. This red label indicates a manufactured home built after June 15, 1976. The absence of this label on a factory-built home suggests either a mobile home (pre-1976) or a modular home.

Examine your home's foundation. Mobile homes and manufactured homes may sit on piers, blocks, or skirting systems, though some are placed on permanent foundations. Modular homes always sit on permanent foundations built to the same standards as site-built homes.

Review your deed and property records. Modular homes are typically classified as real property and taxed as site-built homes. Mobile and manufactured homes may be classified as personal property, especially if they're in rental communities where you don't own the land.

Consider when and how your home was built. If it arrived in multiple large sections that were assembled on-site over a permanent foundation, it's likely modular. If it came as one or two complete units that were placed on the site, it's probably manufactured or mobile.

Your local assessor's office can help clarify your home's classification, as this affects property tax assessment and building code compliance.

Making Informed Insurance Decisions Based on Your Home Type

Understanding your home's classification helps you approach insurance shopping with realistic expectations and appropriate coverage goals.

For mobile homes, focus on carriers that handle older factory-built housing. Be prepared for potentially higher costs and coverage limitations, and consider whether safety upgrades might improve your options.

Manufactured home owners should explore both specialized manufactured home policies and, if applicable, standard homeowners coverage based on their home's foundation type and age.

Modular home owners can shop the full homeowners insurance market, treating their home like any site-built property. This provides maximum coverage options and competitive pricing opportunities.

Working with an agency experienced in factory-built housing helps ensure you get coverage appropriate for your specific situation rather than trying to fit your home into the wrong insurance category.

Understanding the Insurance Implications

The differences between mobile homes, manufactured homes, and modular homes extend beyond terminology in Central New York's insurance market. These distinctions determine your coverage options, affect your premium costs, and influence your ability to secure appropriate insurance coverage.

We covered how mobile homes face the most restrictive insurance market due to age and construction standards, while manufactured homes built to HUD standards have more options available. Modular homes, built to site-built standards, qualify for the full range of homeowners insurance products.

Your home's foundation type, age, and compliance with current standards all play into these distinctions, affecting both your immediate insurance options and long-term coverage considerations.

At the Horan insurance agency, we understand these distinctions and work to match your specific housing situation with appropriate coverage options. Our experience with Central New York's diverse factory-built housing market helps us identify suitable approaches for your circumstances.

Click the Get a Quote button below to discuss your factory-built home and explore insurance options designed for your specific type of construction and situation.

Topics:

{kind=link}