You’ve probably heard the saying, “When it rains, it pours!” In a literal sense, people reach for umbrellas during a downpour. Personal umbrella coverage is so named because it covers you when you’ve used up all the liability coverage on your home, auto, and other policies. It’s that extra layer of protection—the umbrella over and above it all—if or when you need it.

Because the assets you’ve worked hard for are at risk of claims resulting from property damage and personal injury, the coverage offered in other policies is often not enough. Personal umbrella insurance—a practical and more affordable option than you think—starts with $1,000,000 in coverage and goes as high as $5,000,000 or above, depending on your needs.

At first glance, umbrella coverage—also called excess liability coverage—may seem like a hard upsell. You’ve likely experienced this. While reserving seats on a flight, an airline dangled a tempting business- or first-class upgrade so you could avoid sitting in a cramped economy seat between two strangers. Or, your bank lured you with the promise of bonus points and cashback if you signed up for a more premium credit card.

Many people view umbrella coverage similarly and reject it because they misunderstand its purpose and fail to see its benefits. At Horan, we’ve handled umbrella policies for scores of satisfied clients over the past decade, all of whom have more peace of mind because of the added protection. This article will shed light on how umbrella insurance works, what it does and does not cover, and who can benefit from it.

What Does a Personal Umbrella Insurance Policy Cover?

Personal umbrella insurance coverage is broad and sweeping, like a great American novel. In addition to going over and above auto, home, and other policies, umbrella insurance also covers claims those policies don’t.

Personal umbrella insurance coverage is broad and sweeping, like a great American novel. In addition to going over and above auto, home, and other policies, umbrella insurance also covers claims those policies don’t.

You can expect additional liability coverage for bodily injuries, property damage, and certain lawsuits, but there’s more. Let’s dive in.

You’re protected when another person suffers bodily injuries during an accident. Umbrella insurance covers the medical bills and resulting liability claims (if any) beyond the limits of your other policies. Some examples include:

- Auto accidents for which you’re at fault, even if they involve multiple injured parties.

- A guest suffering a spinal injury after falling off your backyard trampoline.

- A guest slipping on the steps during the night and suffering broken limbs and a concussion.

- Your dog causing harm to others (see Limitations section).

You’re also covered when you’re at fault for property damage suffered by another person. One example includes:

- Auto accidents resulting in the loss of multiple vehicles, which your policy must replace.

As a rental property owner, you’ll have additional landlord liability protection above an underlying landlord insurance policy. Whether you rent out a home or apartment unit, some examples include:

- You’re involved in a lawsuit brought by a third party due to damages your tenant caused.

- A tenant sues you for wrongful eviction.

Umbrella insurance covers you in the event of certain lawsuits and the associated costs for legal defense. Some examples include:

- You get into a verbal dispute with someone regarding a hot-button issue, and he sues you for slander.

- You go on social media to fire off a series of heated posts against a neighbor, and she sues you for libel or cyberbullying.

- You falsely arrest or detain someone, and they sue you.

Umbrella insurance can also protect members of your household, such as a teenage son or daughter who lacks years of driving experience and is more likely to encounter auto accidents that lead to liability claims.

And coverage from an umbrella policy can even protect you when traveling outside the US.

What Does a Personal Umbrella Policy Not Cover?

As broad and sweeping as umbrella insurance is, it doesn’t cover everything. But no policy does. And since it’s a liability policy, personal umbrella insurance covers you for property damage or injury caused to others. Excluded are injuries you incur or damage you cause to your personal property. In addition, other losses that fall outside the scope of coverage are:

- Business losses

- Liability involving those who serve on a board of directors of a non-profit organization

- Criminal acts you commit

- Contracts, be they written or oral

- Injuries or damage you or a covered household member cause with intent

- Damage caused by nuclear means, war, or terrorism

- Lawsuits deriving from infectious diseases, such as being sued for giving someone a sexually transmitted disease (STD)

How Personal Umbrella Insurance Works

To understand umbrella insurance better, imagine this scenario. A driver in Central New York travels on I-81 during one of our customary lake-effect winters, and a blizzard creates a sudden whiteout that impedes his ability to see the road and traffic around him.

The driver veers across three lanes, including an on-ramp, and takes out four vehicles along the way, creating a multi-car accident that involves other vehicles. Several people are injured.

He is at fault, and the liabilities total $975,000. But the driver’s auto policy limited bodily injury coverage to $300,000.

If he didn’t have a $1,000,000 personal umbrella policy, he would have to use his savings and investments to pay the remaining $675,000. His $1,000,000 umbrella insurance kicked in after the auto policy met the bodily injury limit.

Your umbrella insurance coverage will function the same way. Here’s a quick breakdown:

- Total Cost of a Multi-Car Accident – $975,000

- Auto Insurance: Bodily Injury Limit – $300,000

- Umbrella Insurance Coverage – $675,000

Who Needs Personal Umbrella Insurance?

One might ask, “Is an umbrella policy a waste of money?” or “Is it just for the wealthy?” These are both excellent questions. After all, who needs personal umbrella insurance?

When insurance surfaces in a conversation, it’s never discussed as a thing of glamour. No one pampers themselves with insurance coverage. It’s a need, not a want.

The problem with insurance is the need for it resides in the future—and we all hope that need remains there. You’re buying peace of mind and protection—“just in case.” And neither is ever a waste of money or just for the wealthy.

How much peace of mind and protection you require depends on your situation, which is personal and unique for each of us.

Say you’re starting out in life and haven’t accumulated many assets or substantial savings. You might say to yourself, “Who cares about a lawsuit? Go ahead, sue me! I have nothing to lose.”

Then you cause a car accident that uses up your liability limits. You think to yourself, I’m fine. The insurance company threw in all my policy was worth, and I have no more money.

Despite what you think, it doesn’t end there. You probably don’t know that a claimant can obtain a court order to garnish your future wages to cover the cost of a past claim that used up your liability limits. And they will garnish your wages (these are automatic deductions from your paycheck) for as long as it takes to pay the entire claim.

Anyone can be subject to wage garnishment.

Another scenario surrounds future life insurance inheritances. You may be at a life stage where you don’t have much money, but one day a close relative may die and leave you a $250,000 life insurance inheritance. If a past claimant renews a judgment against you each year for 17 years, the minute you receive your inheritance, it goes to them.

Therefore, umbrella insurance doesn’t just apply to what you earn now, it also protects what you can earn in the future.

Regardless of your financial situation, there is a small likelihood of facing a court judgment that exceeds the sum of your home and auto policy limits. But the possibility exists.

If this happens, you could lose your entire savings and jeopardize your financial future. Suitable umbrella insurance coverage reduces that risk. So, who needs personal umbrella insurance? Anyone who wants to safeguard their assets and protect their financial future.

What Does Personal Umbrella Insurance Cost?

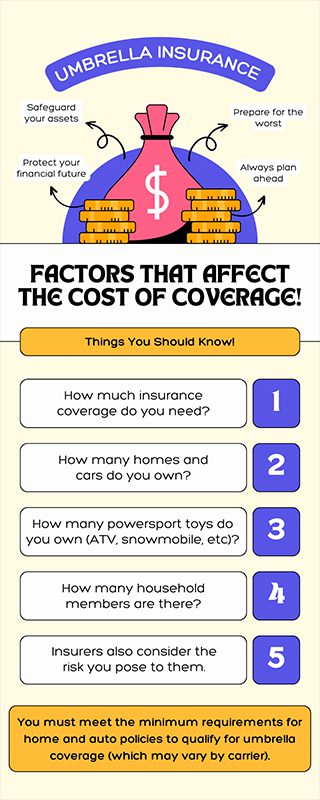

Several factors determine the price of personal umbrella insurance policies. While rates differ from state to state, all insurance companies, including those in New York, will consider the risk you pose to them.

Several factors determine the price of personal umbrella insurance policies. While rates differ from state to state, all insurance companies, including those in New York, will consider the risk you pose to them.

The amount of coverage you intend to purchase also affects pricing, as does the number of homes and cars you own and the total household members on the policy.

However, your additional coverage is affordable compared to other common insurance policies.

The average annual cost of $1 million of umbrella coverage (the base for most insurance companies) is from $150 to $300.

That cost goes up incrementally for each million added up to a point. Adding a second $1 million may cost an extra $75, and a third million may cost $50 more, with each additional million coming at the same rate.

These low rates may surprise you, considering the extensive coverage you’re getting. Insurance companies can afford to price umbrella policies this way because it is, in a sense, an add-on. Depending on whether you rent or own a home or vehicle, existing homeowners, renters, and auto policies must be in place before you can purchase umbrella insurance—and we’re talking about the required liability limits for those policies.

Since you have to increase the limits of your home and auto policies to the required threshold to qualify for umbrella coverage, your premiums will go up. Bear that in mind.

Are There Limitations to Personal Umbrella Insurance?

Due to a 2021 animal welfare legislation package signed by Governor Kathy Hochul, New York insurers can no longer reject or penalize you based on your dog’s breed. But that doesn’t stop them from limiting your dog’s coverage.

But let’s take a step back.

In the past, insurers refused to write homeowner policies for people who owned dogs that fell on a narrow list of suspected notorious breeds. Topping the list are:

- Akitas

- Chow chows

- Doberman pinschers

- German shepherds

- Huskies

- Mastiffs

- Pit bulls

- Presa Canarios

- Rottweilers

- Wolf breeds.

With the new state law, insurance companies can no longer restrict insurance coverage to owners of certain dog breeds. But because those insurers still view the breeds on the list as inherently dangerous, they created a limitation.

Homeowners and renters insurance policies cover liability expenses for dog bites up to limits averaging $100,000 to $300,000. But, for those maligned dog breeds, some New York insurers place further limits on animal liability coverage that bars policyholders from qualifying for personal umbrella insurance. Knowing this info will help you determine whether or not the limitation will affect you.

Protect Your Financial Future

You may feel your current homeowners and auto policies offer adequate protection, and you’ve gotten by fine so far. But none of us can predict the future. The uncertainty ahead doesn’t have to cost you everything you own. It pays to be prepared, which is why we strongly advise many of our clients to purchase personal umbrella insurance as an extra layer of protection.

But if you want to learn other ways to beef up financial protection through your homeowners insurance, see what happens when you add riders to your policy.

If you’re ready to add umbrella policy protection, call 315-635-2095 and speak to one of our insurance specialists to learn about the best options available.

Topics:

{kind=link}