Business owners in Central New York face numerous situations that could lead to lawsuits. Understanding which insurance coverage applies to specific scenarios can make the difference between helping to protect everything you've built and losses that could cripple your operations.

Many clients come to us confused about when general liability applies versus when professional liability is needed.

At the Horan insurance agency, we've noticed this confusion often leads to coverage gaps that leave businesses vulnerable. Our team works with CNY businesses to clarify these distinctions and help identify suitable coverage combinations.

This article breaks down the fundamental differences between general liability and professional liability insurance, helping you determine which type of coverage your business may require.

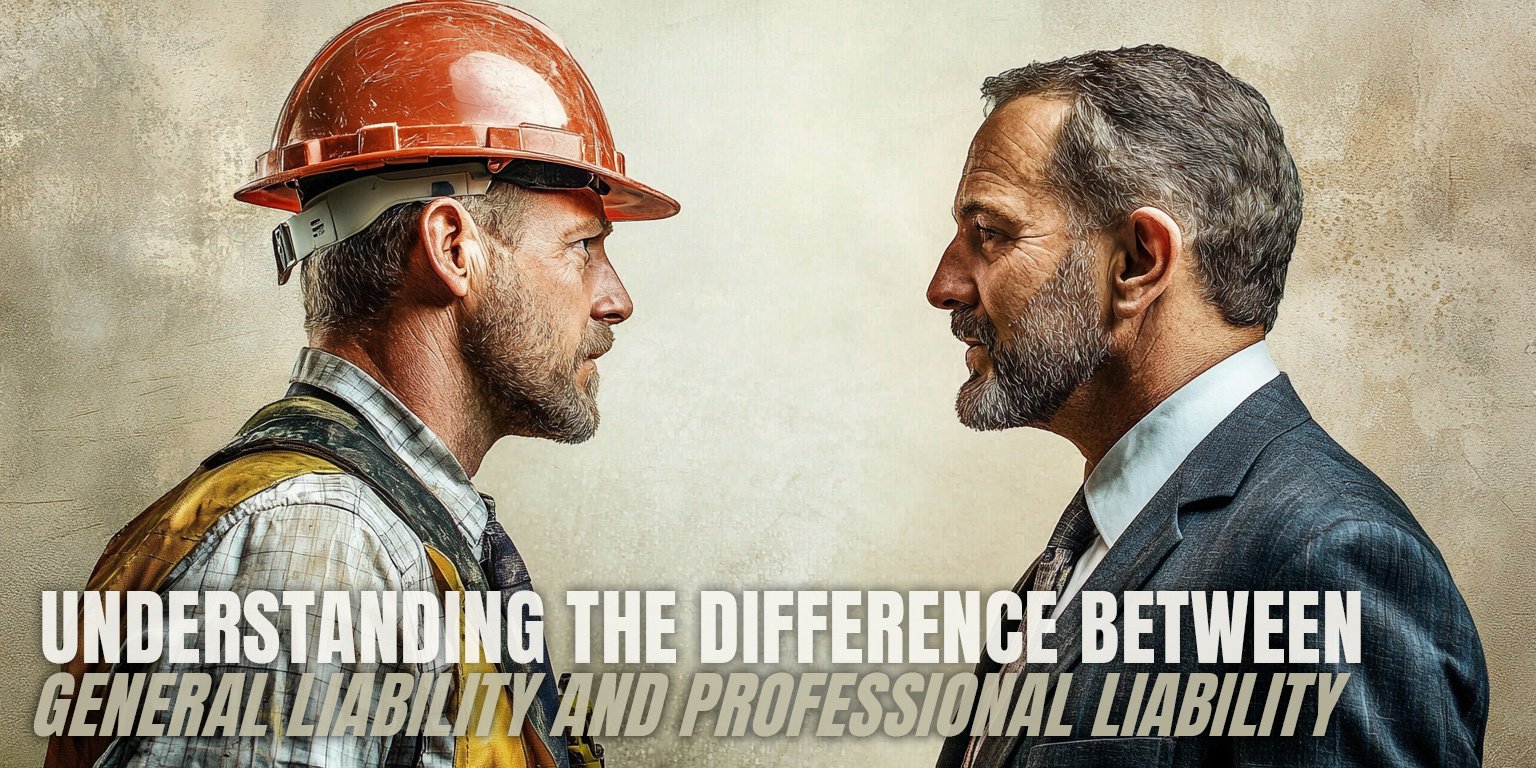

Tangible Harm vs. Service-Related Claims: The Core Insurance Distinction

The primary difference between general liability and professional liability insurance centers on the type of harm they address.

General liability insurance primarily addresses bodily injury and property damage. It functions like "slip and fall insurance" that may cover situations when someone gets physically hurt on your premises or when your operations damage someone else's property.

Professional liability insurance, often called errors and omissions (E&O) insurance, works differently. It may address claims that arise when someone experiences detriment to their business or situation due to your professional advice or services. This coverage responds when clients claim your recommendations or actions led to harmful outcomes.

This distinction becomes clearer when examining specific examples relevant to Central New York businesses.

When General Liability Applies: Real-World Scenarios

When General Liability Applies: Real-World Scenarios

General liability responds to physical incidents involving bodily injury or property damage. Consider these scenarios:

- A customer at your Baldwinsville retail store slips on a recently mopped floor, falls, and breaks their wrist

- While working at a client's home in Liverpool, your employee accidentally knocks over and breaks an expensive vase

- During a community event in downtown Syracuse where your business has a booth, a poorly secured banner falls and hits a passerby, causing a head injury

In each case, the incident involves physical damage or bodily injury. General liability insurance may cover medical expenses, property replacement costs, and legal defense if the injured party sues your business, subject to policy terms and limits.

When Professional Liability Applies: Industry Examples

When Professional Liability Applies: Industry Examples

Professional liability addresses negative consequences stemming from professional advice or services. Here are situations where this coverage becomes essential:

- As an accountant in Camillus, you recommend a tax strategy that results in penalties for your client

- Your IT consulting firm in Manlius recommends software that causes data loss for a business client

- As a beautician in North Syracuse, you recommend a specific hair treatment that causes significant damage and hair loss for your client

These scenarios involve adverse business or personal outcomes due to professional services, rather than physical damage. Professional liability insurance may cover legal expenses and potential settlements when clients claim your professional services caused them these negative results, depending on your specific policy provisions.

Who Needs Professional Liability Coverage?

While almost every business benefits from general liability insurance, professional liability coverage is particularly important for certain professions. Professional liability insurance is vital for businesses offering intangible services or advice that, if flawed, could negatively affect their clients' well-being or operations.

This coverage may be important for:

- Insurance agents who recommend policies

- Accountants who provide tax advice

- Real estate professionals who guide property transactions

- Attorneys offering legal counsel

- Professional Employer Organizations

- IT consultants recommending technology solutions

- Mechanics diagnosing vehicle problems

- Beauticians providing services

- Contractors advising on building materials

Medical professionals typically need a specialized form of professional liability called malpractice insurance, which addresses the unique risks associated with healthcare services.

Specialized Professional Liability for Different Industries

Different industries face unique professional liability risks. Understanding these distinctions helps businesses secure appropriate coverage:

IT Professionals

IT Professionals

IT consultants and service providers face liability when recommending software, hardware, or systems. If these solutions fail to perform as promised or cause data loss, clients may sue for damages. Professional liability insurance designed for technology professionals may address these industry-specific exposures.

Accountants

Accountants

Accountants provide financial guidance that directly impacts their clients' tax obligations and business decisions. Errors in tax preparation or financial reporting can lead to penalties and business losses for clients. Professional liability coverage for accountants may address these profession-specific risks.

Mechanics

Mechanics

Auto repair professionals make diagnostic recommendations that affect both vehicle safety and repair costs. If a mechanic recommends unnecessary repairs or fails to identify critical safety issues, they may face liability claims. Professional liability insurance for mechanics may provide coverage for claims related to their professional judgment.

Documentation: Essential for Both Liability Types

Strong documentation practices help defend against both general and professional liability claims.

For general liability protection:

- Maintain regular safety inspection logs

- Document cleaning procedures and schedules

- Keep records of property maintenance

- Post appropriate warning signs

For professional liability protection:

- Document all client communications

- Use detailed contracts that clearly define scope of work

- Maintain records of client decisions and approvals

- Keep organized files of all project-related documents

When potential claims arise, this documentation provides valuable evidence about what occurred and what was communicated, helping defend against allegations.

Finding Suitable Coverage Options

Most businesses need both general and professional liability coverage, but the specific limits and terms depend on your industry and risk factors.

For example, a retail store with high customer traffic might emphasize general liability coverage, while a consulting firm would prioritize professional liability protection. Many businesses benefit from an approach that includes both coverage types.

When evaluating your insurance needs, consider:

- The specific services you provide

- Your client interaction level (in-person vs. remote)

- Contract requirements from clients or partners

- Industry standards for insurance coverage

- Your risk tolerance and financial resources

Working with a licensed insurance agent familiar with your industry helps identify suitable coverage options for your specific situation.

Understanding Professional Liability Costs

The cost of professional liability insurance varies depending on your profession. For some businesses, policies start at around $300 per year for $1,000,000 in coverage limits. However, higher-risk professions like doctors may pay thousands for protection.

This price difference reflects the varying risk levels associated with different professions. A beautician's professional liability exposure differs significantly from a surgeon's malpractice risk. The premium you'll pay depends on your industry, services provided, claim history, and desired coverage limits.

Help Safeguard Your Business with Appropriate Liability Coverage

Understanding the difference between general liability and professional liability insurance helps ensure appropriate protection for your business. General liability addresses physical harm and property damage, while professional liability covers negative consequences stemming from your advice or services.

Without proper coverage, a single claim could affect your business. Don't leave your business vulnerable to these common risks.

At the Horan insurance agency, we help Central New York businesses identify their liability exposures and find insurance solutions. Our team understands the specific challenges facing local businesses and can guide you toward coverage options.

Click the Get a Quote button below to start securing coverage that addresses both your general and professional liability risks. Our team will help you find solutions that fit your requirements and budget.

Topics:

{kind=link}