Many Central New York businesses and individuals face uncertainty when hiring contractors or service providers. The question keeps surfacing: How can you confirm that the people working on your property or project have adequate insurance coverage?

Without clear verification, you're left wondering whether you might face unexpected liability if something goes wrong. That worry about being exposed to risk—and not knowing if your contractor can handle potential claims—creates real stress for business owners and homeowners alike.

At the Horan insurance agency, we work with Central New York clients who need information about insurance documentation when hiring contractors and service providers. As an independent agency working with multiple carriers, we have insights into how Certificates of Insurance function and why they matter for your situation.

This article explains what a Certificate of Insurance is, who needs one, and how to read the key elements that affect your risk exposure. We'll walk through the document's components, clarify common misconceptions, and show you what to look for when reviewing certificates from contractors or service providers in Central New York.

Jump to Article Section

- Understanding Certificates of Insurance in Central New York Business Relationships

- Who Needs a Certificate of Insurance?

- Why Certificates of Insurance Matter: Verifying Coverage for Your Projects

- How to Read a Certificate of Insurance: Key Elements to Look For

- The Importance of Being a Certificate Holder: More Than Just a Name on Paper

- Common Misconceptions About Certificates of Insurance: Separating Fact from Fiction

- Verify Contractor Insurance Coverage for Your Central New York Projects

Understanding Certificates of Insurance in Central New York Business Relationships

A Certificate of Insurance is more than just a piece of paper—it's your first line of defense in verifying insurance coverage. This document serves as tangible proof that a company or individual has active insurance policies in place. Think of it as a snapshot of their insurance status, giving you a quick overview of their policy types at a glance.

But why does this matter to you? Imagine you're a business owner in Syracuse, hiring a contractor for a major renovation project. Without a Certificate of Insurance, you're left without confirmation of whether the contractor has an active policy to help address potential issues if something goes wrong.

That uncertainty can lead to sleepless nights and potential financial headaches down the road.

When it comes to temporary employment or short-term contracts, Certificates of Insurance are a common requirement. This allows businesses and individuals to verify insurance coverage for specific projects or time-limited engagements without needing to review entire insurance policies.

Who Needs a Certificate of Insurance?

Certificates of Insurance play a vital role in many business relationships across Central New York. Let's break down who typically needs one:

1. Organizations Hiring Contractors

If you're a business owner in Central New York, you'll likely request Certificates of Insurance when hiring:

- Construction contractors for building or renovating your office space

- Cleaning services to maintain your premises

- IT consultants to manage your technology infrastructure

- Event planners for corporate functions

For example, imagine you're planning a major product launch event in downtown Syracuse. You hire an event planning company to handle the details. By requesting a Certificate of Insurance, you confirm that the event planner has general liability coverage if a guest is injured during the event.

This can help address your business exposure to potential lawsuits and financial losses.

Additionally, if your organization frequently hires temporary workers or freelancers, requesting Certificates of Insurance from these individuals or their agencies can help address potential liabilities arising from their work.

2. Individuals Hiring Service Providers

As a CNY homeowner, you should ask for a Certificate of Insurance when hiring:

- Landscapers to maintain your property

- Home renovation contractors for remodeling projects

- Roofing companies for repairs or replacements

- House cleaning services for regular maintenance

Don't hesitate to request this documentation from any contractor you're considering hiring. It's a standard practice and demonstrates your diligence in addressing risk to your property and finances.

3. Businesses Providing Services

3. Businesses Providing Services

If you're a Central New York business offering services to other companies or individuals, you'll often need to provide Certificates of Insurance to your clients. This applies to a wide range of industries, including:

- Construction and contracting

- Consulting services

- Event planning

- Professional services (e.g., accounting, legal)

For instance, if you run a small IT consulting firm in Oswego, potential clients will likely request a Certificate of Insurance before engaging your services. This demonstrates your professionalism and commitment to addressing both your business and your clients' interests.

As a business owner, you should be prepared to request these certificates from your own insurance company. Keep several on hand, as you may need to furnish them frequently to potential clients or business relationships. This proactive approach can help you win contracts and build confidence with your clients.

Why Certificates of Insurance Matter: Verifying Coverage for Your Projects

Certificates of Insurance are more than just bureaucratic paperwork—they're a crucial tool for verifying coverage for both parties in a business relationship. Here's why they matter:

- Verification of coverage: They provide concrete proof that the contractor or service provider has active insurance. This eliminates the guesswork and reduces your exposure to risk.

- Risk management: By verifying insurance coverage, you can help address potential liability if something goes wrong during the project. This can help you avoid costly legal battles and financial losses.

- Professionalism: Providing or requesting a Certificate of Insurance demonstrates business acumen and responsibility. It shows that you take your obligations seriously and are committed to addressing concerns for all parties involved.

- Compliance: In some industries or for certain projects, having a Certificate of Insurance may be a legal or contractual requirement. Failing to obtain one could put you in breach of regulations or agreements.

- Financial protection: If an incident occurs and the other party's insurance is inadequate or non-existent, you could be held liable for damages. With a Certificate of Insurance, you're less likely to be the first in line to cover the financial fallout from someone else's mistake.

Consider this real-world example: You're a restaurant owner in Baldwinsville, hiring a plumbing company for some repairs. During the work, a plumber accidentally causes water damage to your dining room.

If the plumbing company has general liability insurance (verified by their Certificate of Insurance), their policy may cover the damages. Without it, you might be stuck with costly repairs and lost business.

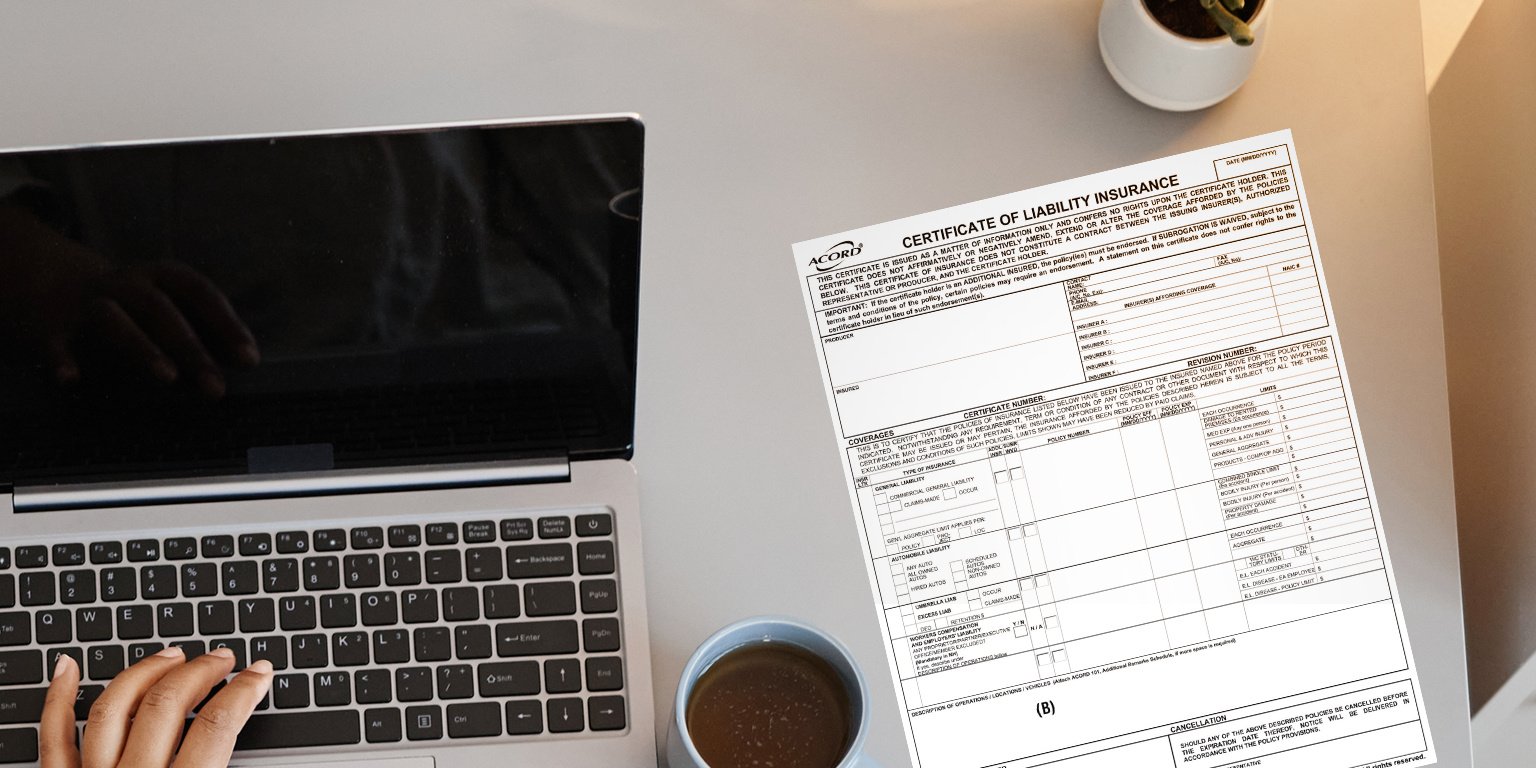

How to Read a Certificate of Insurance: Key Elements to Look For

When you receive a Certificate of Insurance, it's crucial to know how to interpret the information. Here are the key elements to focus on:

- Policy effective dates: Ensure the coverage is current and will remain active throughout your project. Look for both the effective date and expiration date of each policy listed.

- Types of coverage: Check for the specific types of insurance relevant to your project. Common types include:

- General Liability

- Workers Compensation

- Professional Liability (also known as Errors and Omissions)

- Automobile Liability (if vehicles are used in the work)

- Coverage limits: Verify that the limits meet your requirements or industry standards. This typically includes:

- Per occurrence limit: The maximum amount the insurer will pay for a single incident

- Aggregate limit: The total amount the insurer will pay for all claims during the policy period

- Additional insured status: If applicable, confirm that your business is listed as an additional insured. This status can provide additional coverage to you under their policy if claims result from work they perform for you.

- Policy numbers: These unique identifiers can be used to verify the policy with the insurance company if needed.

- Insurance company information: Check that the policies are issued by reputable, financially stable insurance companies.

Let's put this into context with a Central New York scenario: You're a property manager in Auburn, hiring a snow removal company for the winter. When reviewing their Certificate of Insurance, you'd want to verify:

Let's put this into context with a Central New York scenario: You're a property manager in Auburn, hiring a snow removal company for the winter. When reviewing their Certificate of Insurance, you'd want to verify:

- The policy is effective throughout the winter months

- It includes general liability and workers' compensation coverage

- The liability limits are adequate (typically at least $1 million per occurrence)

- Your property management company is listed as an additional insured

- It is signed by the carrier or agency rep

By carefully reviewing these elements, you can make informed decisions about the businesses you work with and better understand your risk exposure.

The Importance of Being a Certificate Holder: More Than Just a Name on Paper

When you're hiring a contractor or service provider, it's crucial to be listed as a certificate holder on their Certificate of Insurance. This status offers several important benefits and is distinctly different from simply receiving a copy of the certificate:

- Direct notification: As a certificate holder, you may have the option to receive updates if the policy is canceled, non-renewed, or altered. This keeps you informed about any changes that might affect your risk exposure. If you're not listed as a certificate holder, you might not be notified of these changes.

- Verification: Being listed as a certificate holder confirms that the insurance agency has indeed issued the certificate. This reduces the risk of fraudulent documentation and gives you added assurance of the coverage's validity.

- Documentation: Your status as a certificate holder provides a paper trail, which can be invaluable if you need to make a claim or prove due diligence in verifying insurance coverage.

- Customized information: The certificate will often include specific information about your project or relationship with the insured party, making it more relevant and useful for your needs.

- Stronger confirmation of active insurance: Being listed as a certificate holder can provide stronger confirmation of active insurance coverage. Insurance agencies won't issue a certificate listing you as a holder if the policy is in arrears or has been canceled or non-renewed. This provides an extra layer of assurance that the coverage is current and valid.

Common Misconceptions About Certificates of Insurance: Separating Fact from Fiction

There are several misconceptions about Certificates of Insurance that can lead to misunderstandings and potential risks. Let's clear up some of these misunderstandings:

- It's not a policy: A Certificate of Insurance summarizes coverage but doesn't replace the actual insurance policy. It doesn't provide coverage on its own.

- It's not a guarantee: While it shows active coverage at the time of issuance, it doesn't guarantee future coverage. Policies can be canceled, non-renewed, or altered after the certificate is issued.

- It's not always comprehensive: Some Certificates of Insurance might not list all coverages or exclusions. It's a summary, not a complete policy document.

- Additional insured status isn't automatic: Being listed as a certificate holder doesn't automatically make you an additional insured. This requires specific endorsement on the policy.

- It doesn't alter the policy: A Certificate of Insurance is informational. It doesn't change the terms or conditions of the actual insurance policy.

Understanding these points can help you avoid potential pitfalls. For example, a contractor in Oneida might provide you with a Certificate of Insurance at the start of a project, but if their policy is canceled or non-renewed midway through, you could be exposed to risk.

Regular verification and communication with your contractors about their insurance status is vital.

Verify Contractor Insurance Coverage for Your Central New York Projects

Verify Contractor Insurance Coverage for Your Central New York Projects

Whether you're a business owner in downtown Syracuse or a homeowner in the suburbs of Oswego, Certificates of Insurance provide a way to verify that contractors and service providers carry active insurance coverage.

By requesting and correctly interpreting Certificates of Insurance, you're taking steps to confirm coverage exists for your business or personal projects. You're working to verify that if something goes wrong, you've addressed some vulnerability to financial losses or legal complications due to someone else's lack of coverage.

Consider implementing these practices:

- Request Certificates of Insurance before beginning work with new contractors or service providers.

- Review your certificate requirements to confirm they align with current industry standards and your situation.

- Keep records of all Certificates of Insurance, including expiration dates, so you can follow up when renewals are needed.

- Work with an insurance agency that can provide information about the process and help you understand different types of coverage.

At the Horan insurance agency, we work with Central New York businesses and individuals on insurance documentation questions. Our access to multiple carriers gives us perspective on Certificates of Insurance and how they fit into risk management approaches.

We can assist you with:

- Understanding what to look for in a Certificate of Insurance

- Determining coverage limits for your situation

- Implementing a system for tracking and managing Certificates of Insurance

- Addressing questions about your insurance documentation

When you understand how to request and review Certificates of Insurance, you're taking steps to verify coverage exists before work begins. This documentation helps you confirm that contractors carry insurance, which can help address your exposure to risk from their operations.

Click the Get a Quote button below to connect with our team and learn how we can help you use Certificates of Insurance to verify contractor coverage and address risk exposure for your business or personal projects.

Also be sure to read: The Importance of Being Listed as an Additional Insured on CNY Policies.

{kind=link}