Many New York drivers pay for no-fault insurance every month without knowing what it covers or how to use it when they need it most. The confusion starts with the name itself—despite being called "no-fault," this coverage has nothing to do with determining who caused an accident. Instead, it focuses on getting you the medical care you need regardless of fault.

At the Horan insurance agency, we've helped many Central New York drivers understand their no-fault coverage since 2009. We find that clear information about this mandatory coverage helps our clients make confident decisions when filing claims after an accident.

This article will guide you through the practical aspects of using your no-fault benefits, from identifying what you currently have to understanding when and how to access these benefits after an accident.

What Your No-Fault Insurance Actually Covers in New York State

What Your No-Fault Insurance Actually Covers in New York State

No-fault insurance in New York isn't an optional coverage—if you have registered vehicles with plates, you have this protection. Also known as Personal Injury Protection (PIP), no-fault insurance covers medical expenses for you and your passengers after an accident.

The term "no-fault" indicates that regardless of who caused the accident, each person involved uses their own insurance company for medical expenses. This coverage becomes your primary medical coverage after an auto accident, taking precedence even over your health insurance plan.

When you visit a healthcare provider for accident-related injuries, they'll request your auto insurance information first—not your health insurance card. This arrangement helps expedite treatment without waiting for fault determination.

The basic no-fault package includes:

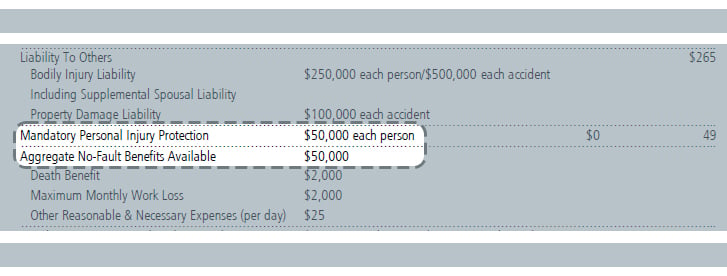

- Medical expense coverage up to $50,000 per vehicle occupant

- Income replacement at 80% of lost wages (up to $2,000 monthly)

- $25 daily allowance for other necessary expenses

- A $2,000 death benefit

No other coverage in your auto policy works quite this way, which contributes to the confusion many drivers experience when trying to understand their benefits.

Learn more about how no-fault insurance works in Central New York.

Accessing Additional No-Fault Benefits Beyond the Basic Coverage

The standard $50,000 in no-fault coverage serves as your foundation, but many Central New York drivers find this basic protection insufficient for serious injuries. New York allows you to increase your protection in two ways:

- Additional Personal Injury Protection (APIP) lets you purchase extra coverage, typically sold in $50,000 increments up to $100,000 beyond the basic amount. This expanded coverage provides crucial protection for serious injuries that might exceed the basic $50,000 limit.

- Optional Basic Economic Loss (OBEL) adds $25,000 in flexible benefits that can be directed toward either additional medical expenses or lost wage replacement. This flexibility proves valuable when recovery extends beyond initial expectations.

For example, if Frank commutes daily on I-81 through Syracuse during winter weather, the additional protection could prove valuable if he's injured in a multi-vehicle accident and faces extended recovery time.

These additional coverages provide two key advantages:

- Portability: Your additional benefits travel with you even when riding in someone else's vehicle

- Extended protection: The coverage applies to out-of-state passengers traveling with you

When considering these options, review your current health insurance deductibles and coverage limits. If you have high-deductible health insurance or limited disability coverage through your employer, the additional no-fault benefits become even more valuable.

How to Find Your Current No-Fault Coverage Level

To determine your current no-fault protection level, locate your auto insurance declarations page. Look for the section labeled "Personal Injury Protection" or "No-Fault Coverage."

Within this section, search for the word "aggregate" followed by a dollar amount. This figure represents your total no-fault benefit limit. If you see only $50,000, you have the basic mandatory coverage. If you see a higher number, you've purchased additional protection.

The declarations page should also indicate if you've added the OBEL coverage, which appears as a separate $25,000 benefit.

Many Central New York drivers discover during this review that they don't have the level of protection they assumed. If you're unsure how to interpret your declarations page, contact your insurance representative for clarification.

Many Central New York drivers discover during this review that they don't have the level of protection they assumed. If you're unsure how to interpret your declarations page, contact your insurance representative for clarification.

When Your No-Fault Benefits Won't Apply

While no-fault insurance provides valuable protection, certain situations fall outside its coverage:

- Injuries sustained while driving under the influence

- Injuries resulting from intentional actions or while committing a felony

- Accidents involving motorcycles (which follow different rules in New York)

- Medical expenses beyond your coverage limits

Understanding these exclusions helps you avoid surprises when filing a claim. For instance, a driver who causes a collision on Erie Boulevard after leaving a bar might find their no-fault benefits denied if intoxication contributed to the accident.

Utilizing Your No-Fault Benefits After an Accident

When you're involved in an accident, time becomes critical for accessing your no-fault benefits. You must file your application for benefits within 30 days of the accident to preserve your rights to this coverage.

Follow these steps to help access your benefits:

- Notify your insurance company immediately after any accident

- File with the correct insurer: your own insurance if you were driving your car, the vehicle owner's insurance if you were a passenger, or the vehicle's insurance that struck you if you were a pedestrian or cyclist

- Complete the no-fault application forms (NF-2 form) thoroughly

- Submit all medical bills directly to your auto insurance carrier first

- Track your accident-related expenses, including transportation to medical appointments

- Document lost work time with letters from both your employer and physician

Keep in mind that your health insurance becomes secondary coverage, only activating after you've exhausted your no-fault benefits or for expenses not covered by no-fault. This coordination between insurers requires careful documentation to avoid payment delays.

Understanding Your No-Fault Coverage Options

Understanding Your No-Fault Coverage Options

Understanding how to use your no-fault insurance gives you an advantage after an accident. With this knowledge, you can access medical care immediately without waiting for fault determination and receive financial support during recovery.

The licensed agents at Horan can review your current coverage and explain how additional no-fault benefits might address your individual circumstances. We can help you understand the coordination between your auto insurance, health insurance, and other coverages to explore protection options that fit your situation.

Don't wait until after an accident to learn about these benefits. Take control of your coverage by clicking the Get a Quote button below to discuss your no-fault insurance options.

Understanding your no-fault benefits is just one part of the post-accident process. To learn about the other essential insurance steps, read our article: What Insurance Steps Should You Take if You're in a Car Accident?

Topics:

{kind=link}