When you decide it's time to shop for auto insurance, the first thing most people notice is how much personal information they have to hand over before they receive a single number. If you have multiple drivers and vehicles in your household, the list grows fast. It's a reasonable source of frustration — and it can lead to shortcuts that produce inaccurate quotes.

At the Horan insurance agency, we work with Central New Yorkers on auto coverage every day. We understand that the quoting process feels like a lot of paperwork before you get to the part you actually care about. But every piece of information an agent asks for has a direct effect on the accuracy of your quote — and an inaccurate quote can cause real problems down the road.

In this article, you'll learn what personal information is required for an auto insurance quote and why each item matters. Having this information ready before you contact an agent will move the process along and get you to a number you can actually rely on.

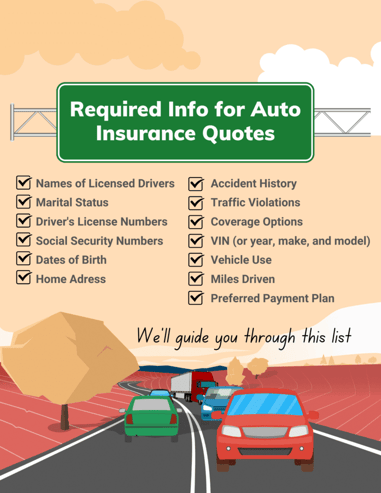

Types of Personal Information Required for an Auto Insurance Quote

Names of All Licensed Drivers

The legal names of all licensed drivers must be provided. This includes drivers who have separate insurance. It also includes drivers who do not have a vehicle of their own but are still licensed.

And make sure you add "Jr" or "III" for individuals with those suffixes. That way, if Thomas Sr had a speeding ticket, it wouldn't be applied to Thomas Jr by mistake, who drives responsibly.

Marital Status

Married drivers tend to receive lower rates. Marital status also serves as a check and balance. If you’re married, but your spouse lives at a different address, you’ll give extra information about this.

Separated couples, who are not yet divorced, also need to disclose that fact. A separated marital status indicates that there is a spouse who lives elsewhere.

Driver’s License Numbers

If the license is a New York one, then you’ll give the 9-digit driver’s license number for each person. It’s okay if you or someone else has an out-of-state license. You’ll need to have the unique ID number and know its state!

The driver's license numbers give an agent access to specific information — including the motor vehicle report for each driver, which an agent needs to sell a policy.

Social Security Numbers

The social security numbers (SSN) are for the one or two individuals who will be the policy owners. Policy owners are also called Named Insureds. The SSN links to information about your financial and insurance claims history.

It’s essential to set the record straight on those two points. The financial history, in particular, is not about your credit score. In fact, it’s not a hard credit pull and doesn’t show up on your credit report. It's also not something we see details about on our end. The information runs through the process behind the scenes, and the outcome factors into the final insurance cost.

It’s essential to set the record straight on those two points. The financial history, in particular, is not about your credit score. In fact, it’s not a hard credit pull and doesn’t show up on your credit report. It's also not something we see details about on our end. The information runs through the process behind the scenes, and the outcome factors into the final insurance cost.

With all else being equal, our experience has shown that those with less debt tend to have lower insurance premiums.

Dates of Birth

Since age plays a significant role in insurance rates, the date of birth (DOB) for every driver is mandatory. Be sure to know the exact one for every driver.

Home Address

You’ll need your current address and any other home addresses within the past three years. Your address establishes precisely where your vehicles are kept. If one or more of your cars are kept elsewhere, you’ll be asked for that address too.

Your mailing address can be different from your street address. Yet, the street address must also be provided because you still can’t fit a car into a PO Box since last we checked.

Your Driving, Accident, and Insurance History

Tickets and Accidents

Insurance carriers will review the past five years of driving history for each driver. Any accidents or tickets should be disclosed. Even if you were not at fault in the accident, you still want to mention it. Doing so will help keep you from being negatively rated for an accident you did not cause.

Current Insurance Coverage

Your current insurance coverage provides us with insight into your policy and premium. We’ll ask for the name of your insurance company. That way, if it’s a carrier we also use, we won’t include them when sourcing quotes.

For accurate comparisons, knowing your current coverage is valuable. If you have $250 deductibles on your existing policy, we wouldn't want to use $500 in your quote. Our goal is to match or improve what you have now.

You can email us your policy’s coverage pages to make things easy.

What if I Don’t Have Insurance?

But suppose you are not currently insured or have been uninsured for more than 30 days. In that case, the availability of auto insurance carriers will be fewer. However, as an independent insurance agency, we work with insurers that can help us in this area.

Details About the Vehicles

Which Vehicles Do You Want to Insure?

Now we get to the vehicle itself — the reason you're here in the first place.

The easiest way for us to locate accurate information about your vehicles is to provide us with something called the VIN. VIN stands for “vehicle identification number,” and every vehicle in the United States has one. Cars or trucks manufactured after 1980 have a 17-character VIN.

You’ll find the VIN in several places throughout the vehicle. But the most common place is on the lower-left corner of your dashboard in front of the steering wheel.

While VINs eliminate the likelihood of a change in the quoted rate, we can still help if you don’t have them. The year, make, and model go a long way toward providing an accurate quoted rate. Knowing it’s a 2019 Honda Pilot EX-L instead of just a “newer-ish Honda SUV” makes a big difference!

How the Vehicle is Used

How far is your commute to work? Are you a stay-at-home mom? Are you a REALTOR® who uses a car when showing houses? Do you drive for Uber? Those are the types of questions you’ll be asked to answer about how each vehicle is used.

Annual Miles Driven

You will need to know how many miles per year are added to each vehicle. While every carrier has its own threshold, vehicles that are driven less than 7,500 miles per year usually get lower rates.

Your Preferred Way of Paying for Auto Insurance

Payment Plan

Your payment plan could end up being the ultimate differentiator. Insurance companies use their payment plans as an added competitive measure. Depending on your specific insurance plan, sizeable auto insurance discounts may be available.

The most common plans include:

- Paid in Full (the entire premium paid in one lump sum).

- Monthly EFT (your payments are automatically drawn from your checking account).

- Monthly Bill. This means you receive a paper (or electronic) bill and manually pay it by personal check, a credit card, or through your bank’s bill pay system.

We Can Help You Get Accurate Auto Insurance Quotes

Getting an accurate auto insurance quote doesn't have to feel like an obstacle course. When you come prepared with the right details — your license numbers, vehicle information, driving history, and payment preferences — the process moves quickly, and the quote you receive reflects your actual situation. That means fewer surprises at the closing stages of your policy and a price you can plan around.

Without that preparation, quotes can shift after the fact. A missing driver, an undisclosed accident, or an unknown VIN can all cause the number to change — sometimes significantly. That kind of uncertainty creates delays and can affect your decision-making.

At the Horan insurance agency, we work with multiple carriers across Central New York and bring that perspective to every quote. We'll ask the questions that matter, help you sort through the details, and work to find coverage options that fit your situation.

Click the Get a Quote button below to get started.

Topics:

{kind=link}