Hiring a subcontractor who can deliver on time and on budget is hard enough. Knowing whether they carry suitable coverage is a different kind of challenge — and one that catches many Central New York contractors off guard. When something goes wrong on a job site, the question of who holds insurance determines who holds the bill.

An uninsured subcontractor doesn't just risk their own losses. They can draw your policy, your client relationship, and your reputation into a dispute you didn't start and didn't budget for. That exposure is more common than most contractors expect.

The Horan insurance agency has been working with contractors across Central New York since 2009. We understand the pressure of managing jobs, crews, and compliance — and we've helped many contractors put subcontractor insurance requirements in place before a problem forces the issue.

This article covers the top five reasons to require subcontractors to carry their own insurance, and why doing so is a sound risk management strategy for any CNY contractor who hires outside help.

Reason #1: Contractors Need to Avoid Extra Risks and Liabilities

As a contractor, you’ve insured your business and done the right thing. You’ve done your due diligence and found suitable insurance for yourself. Why would you hire a subcontractor who hasn’t done the same? Why would you take on unnecessary risk for someone who your insurance is not meant to cover? Someone you know nothing about.

You have no idea what their insurance history or loss history is. But you do want to know if they have insurance. So the first reason to require subcontractors to have their own insurance is to cover your own business.

Subcontractors are not employees. If you wanted to hire them as W2 workers, you could cover them on your insurance. But that’s not what a subcontractor is by definition.

You Could Be Left Paying for Damage You Didn’t Cause

Imagine you hire a flooring subcontractor to install hardwood floors in your client’s kitchen, but they do a terrible job. They use the wrong type of wood, cut it unevenly, and leave gaps and exposed nails everywhere. Now, you’re facing a tripping hazard and a code violation.

But wait, it gets worse! The subcontractor, who you didn’t have time to properly vet, doesn’t have flooring insurance and wasn’t part of your original contract with the client. Your client is furious and threatens to sue you for breach of contract.

This is exactly why requiring subcontractors to carry their own insurance is crucial. They’re independent businesses responsible for their actions, and if something goes wrong on the job, their insurance should cover the damages, not yours.

Think of it this way: subcontractor insurance acts as a safety net, keeping you from facing unexpected financial burdens and legal headaches. It ensures everyone plays by the rules and operates with clear financial boundaries.

By requiring your subcontractors to have insurance, you’re essentially saying: “Hey, I trust you to do a good job, but accidents happen. Let’s make sure we’re both covered if something unexpected comes up.”

It’s a win-win situation for everyone involved. You have stability knowing you have coverage in place, and your subcontractors can focus on doing their job without worrying about leaving you with a financial mess.

So, the next time you hire a subcontractor, make sure they have their own insurance. It’s a small step that can save you a lot of trouble down the road.

Reason #2: Contractors Need to Maintain Their Client Relationship

You have a contract with your client. You and your client have agreed on the work, the cost, and the expectations. Your client has no relationship with your subcontractor. Unless your subcontractor has made a separate deal with your client, which is unlikely, your client only trusts you to do the job.

What usually happens is that you hire subcontractors to help you with the work. You might hire

- painters,

- plumbers,

- electricians,

- carpenters,

- flooring experts,

- and so on.

You tell them what to do and agree on payment terms. You don’t involve your client in this process. But what if your subcontractor is uninsured and gets injured on the job? Now you have a big problem. You’ve breached your contract with your client.

Your client has no obligation to the subcontractor. The subcontractor has no protection from you or your insurance. The subcontractor can sue anyone they want. They can sue your client, which will ruin your reputation.

Now say you hire an uninsured electrician for a project and they get injured on the job. Since they lack workers compensation, they might seek compensation from any available source, including:

- Your client’s homeowners insurance: This could trigger a contractual breach, as your agreement with the client likely stipulates that you, the contractor, hold responsibility for any damages or injuries incurred during the project. Not only does this strain your client relationship, but it also exposes them to unnecessary financial burden.

- Your general liability insurance: While meant to cover general risks, it wasn’t designed to handle subcontractor-related injuries. Using it for this purpose could violate policy terms and potentially lead to claim denials.

By requiring subcontractors to have their own insurance, you effectively avoid these risks:

- Subcontractors secure workers compensation, ensuring they receive proper care without involving your client or your insurance.

- It shields you from contractual breaches and potential lawsuits from clients by clearly outlining responsibility for any mishaps.

Reason #3: Contractors Need to Avoid Subcontractor Disasters

Your subcontractor might also bring more people to help him. But those workers aren’t subs, they’re just helpers. Regardless, they’re still your problem. You’re responsible for everyone who works on your project. You have vicarious liability for all their actions. And you’re risking a lot by letting them in. The sub or his helpers might not get hurt, but they might cause damage to the property.

Imagine this: You hire a plumber named Bill for a bathroom remodel in Rome, New York, trusting he has insurance. Turns out, he doesn’t. His “helpers” do shoddy work, causing a major leak that floods the client’s basement and ruins valuables. You're stuck with the mess, costly repairs, and a furious client.

Uninsured subcontractors are liabilities, not assets. Requiring their own insurance shields you from:

- Financial burdens: You won’t be the first line of defense for their mistakes.

- Client headaches: You maintain trust and avoid contractual breaches.

- Legal troubles: Responsibility stays with them, not you.

Cover yourself, your business, and your clients. Insist on subcontractors getting their insurance.

Reason #4: Contractors Need to Comply with Workers Comp Laws

You have to be careful with this one. It can get you in trouble if you don’t follow the rules. Especially in New York State. If you work for commercial clients, they will ask you to have workers comp insurance. If you don’t, they’ll have to put you on their policy. And they don’t want to do that for two reasons:

- It’s expensive.

- Their policy isn’t designed for it and will lead to a likely non-renewal by their insurance provider.

So you get your own workers comp insurance. But it’s not cheap for contractors. And you have to make sure your subs have workers comp too. You can’t hire an uninsured sub without workers comp. That would break your contract with your commercial client.

You agreed to have workers comp for everyone who works on the project. If you bring in people who don’t have it, you’re in breach of your contract. And you’re risking a lot of problems. This is another reason why you need to require subcontractors to have their own insurance.

It keeps you from breaching your contract with your commercial client. And it keeps you from breaking the workers comp laws.

Reason #5: Being Added as an “Additional Insured” on Your Subcontractor’s Insurance

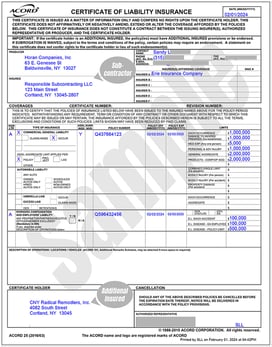

While your subcontractor should have their own insurance, you should be added to it as an additional insured and a certificate holder. They must have insurance for you to do that.

In a sense, you’re their client, and you want to be on their insurance. You want to have control and a clear picture of their coverage. And you want to make sure their policy is active and valid.

In a sense, you’re their client, and you want to be on their insurance. You want to have control and a clear picture of their coverage. And you want to make sure their policy is active and valid.

The only way to do that is to be added to their policy when they request it. A certificate of insurance is not enough. A certificate can be outdated. You want to say, put me on the policy as an additional insured. I want to see my name on it as a certificate holder.

This gives you an added layer of coverage as the contractor against lawsuits and injuries. If something goes wrong on the job site, you have additional coverage in place.

Require Subcontractor Coverage Before a Claim Forces the Issue

Require Subcontractor Coverage Before a Claim Forces the Issue

We covered five reasons why insured subcontractors matter — from maintaining client confidence to complying with New York’s workers comp requirements. Left unchecked, these aren’t abstract risks. They’re the kind of disputes that draw your policy in, delay your projects, and damage relationships you’ve worked hard to build.

Requiring subcontractors to carry their own liability and workers comp coverage isn’t a luxury. It’s a practical measure that gives you composure and stability when something goes sideways on a job. It puts clear financial boundaries in place for everyone involved.

The Horan insurance agency has worked with Central New York contractors since 2009. We can help your subcontractors understand what coverage they need — and help you put requirements in place that hold up. Click the Get a Quote button below to start the conversation..

Topics:

{kind=link}