Owning commercial property in Central New York comes with real financial responsibility. You've invested in a building, signed leases, and counted on rental income — but a fire, a burst pipe, or a slip-and-fall on your property can create significant costs and legal exposure, whether your units are occupied or vacant.

At the Horan insurance agency, we work with commercial property owners across CNY on lessor's risk insurance questions. We work with several carriers to help property owners explore coverage options that fit their situation.

In this article, we'll cover how lessor's risk insurance works, why vacant properties need it too, how construction type affects your premium, and what steps you can take to help manage your insurance costs.

How Lessor’s Risk Insurance Works

As a commercial property owner, you have a unique situation. Let’s say you don’t operate your own business at your Syracuse property. Instead, you lease it to other businesses. This means you need a special kind of insurance: lessor’s risk insurance.

This is the only insurance that covers your property from damage or liability caused by your tenants.

But while you want to make sure the property you rent to other businesses is insured, you also want to make sure your tenants have their own insurance.

They should have liability coverage for their part of the property. But their policy will be secondary to yours. This means that if something happens to your property, you’re the first one to get paid. You don’t want to lose your asset or rental income.

You want to have your property restored as soon as possible and avoid any interruption in your business. Lessor's risk insurance can be an important part of your coverage plan. It can cover your property and liability, and may provide security as a commercial property owner.

Why Lessor’s Risk Insurance is Important for Vacant Properties

Lessor’s risk insurance is not only for properties with tenants. It’s also for properties without tenants. You may have a vacant property for various reasons.

- You may be looking for new tenants.

- You may be renovating the property.

- You may have just bought the property.

Whatever the reason, you still need lessor’s risk insurance.

You’re the only one responsible for your property. You want to help protect it from damage or liability. Many commercial property owners make this mistake. They don’t insure their vacant properties sufficiently. They have policies with big exclusions and fail to cover vacant properties for long periods or even from the start.

This can cause problems for you. You may lose your property or your money. You may face legal issues or miss out on opportunities.

But lessor’s risk insurance can help keep your business running.

How to Avoid Vacancy Surcharges on Lessor’s Risk Insurance

Lessor’s risk insurance isn’t cheap. But there are ways to avoid overspending on your policy. For one, you want to avoid vacancy surcharges. These are extra fees that insurance carriers charge for vacant properties. They can be as high as 50 percent of the policy premium. They apply when your property is vacant for more than 30 or 60 days.

Having tenants in your property helps you avoid these surcharges. But make it a point to show proof of occupancy to your insurance carrier as soon as possible. You want to have signed leases ready to go.

Doing this will help you avoid vacancy surcharges which lowers your insurance costs. This will help you maximize your profits as a commercial property owner.

How to Choose Suitable Tenants for Your Property

Lessor’s risk insurance isn’t only about your property. It’s also about your tenants. You want to choose suitable tenants for your property and avoid tenants that may cause trouble.

Some tenants may have risky businesses, such as nightclubs, strip clubs, tattoo parlors, or other venues that may attract lawsuits, harm, or drunkenness. Some insurance carriers may not prefer these tenants and likely won’t insure your property if you have them. They may consider these tenants outside of their market due to associated risk.

You don’t want to lose your insurance because of your tenants. You want to have tenants that are compatible with your insurance carrier, ones they will consider safe and reliable. You want to have tenants that will help you keep your lessor’s risk insurance.

How to Avoid Vicarious Liability as a Commercial Property Owner

Vicarious liability is when you are responsible for someone else’s actions. This can happen to you as a commercial property owner. You may have tenants who don’t have good or continuous insurance of their own. They may cause damage or injury on your property.

These tenants may not be able to pay for it, which leaves you footing the bill. This is because you own the property. That means you have liability for what happens there, even if it’s not your fault. And the fact that you don’t own the business doesn’t matter. This can be a big problem for you and may cause you to lose money or face lawsuits.

You may damage your reputation or your relationship with your tenants. A lessor's risk insurance policy may help you address vicarious liability exposure. It can help cover costs arising from someone else's mistakes.

But a lessor’s risk policy may not be easy to obtain. It may depend on the type of tenants you have or the condition of your property. Also factor in the availability of insurance carriers.

We can help you determine whether a lessor’s risk policy is obtainable for your commercial property. Contact us for a free consultation.

How the Construction Type Affects Your Lessor’s Risk Insurance

Lessor’s risk insurance is based on the replacement cost of your building. This is how much it would cost to rebuild your building if it was destroyed in a covered peril. The replacement cost depends on the construction type of your building, meaning what your building is made of.

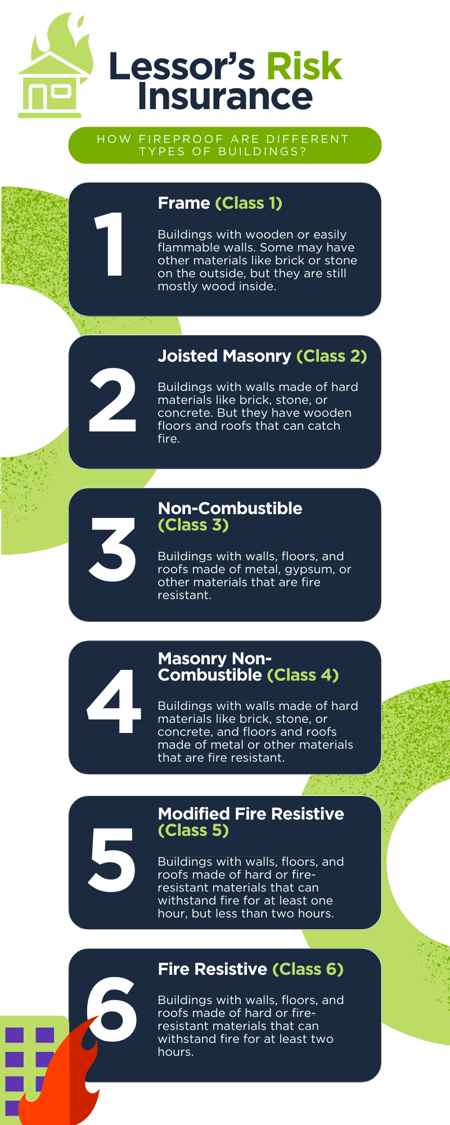

There are different types or classes of construction, which are

- frame,

- joisted masonry,

- non-combustible,

- masonry non-combustible,

- modified or semi fire resistive, and

- fire resistive.

These types have different levels of fire resistance and durability. They also have different impacts on your insurance premium. The premium is the amount you pay for your insurance.

Class 1: Frame Construction

Frame buildings are made of wood or other combustible materials. They’re cheaper to rebuild, but they burn faster and easier. Frame buildings have a higher risk of fire damage and loss, which leads to a higher insurance premium.

Class 2: Joisted Masonry Construction

Joisted masonry buildings are made of concrete or brick walls with wood floors and roofs. They are more expensive to rebuild, but they are more fire resistant than frame buildings. They have a lower risk of fire damage and loss. They also have a lower insurance premium.

Class 3: Non-Combustible Construction

Non-combustible buildings are made with metal, gypsum, or other non-flammable walls, floors, and roofs. They are cheaper to rebuild than masonry buildings, but they are less fire resistant. They have a moderate risk of fire damage and loss and come with a moderate insurance premium.

Class 4: Masonry Non-Combustible Construction

Masonry non-combustible buildings are made of concrete or brick walls and floors with metal roofs. They are even more expensive to rebuild, but they are very fire resistant. They have a very low risk of fire damage and loss and come with a very low insurance premium.

Class 5: Modified or Semi Fire Resistive Construction

Modified or semi fire resistive buildings have hard or fire-resistant walls, floors, and roofs that can withstand fire for at least one hour, but less than two hours. They’re very expensive to rebuild but are extremely fire resistant. They have a very low risk of fire damage and loss, which results in lower insurance premiums.

Class 6: Fire Resistive Construction

Fire resistive buildings are made of reinforced concrete or steel with fire-resistant materials that allow them to withstand fire for at least two hours. They are the most expensive to rebuild. They have the lowest risk of fire damage and loss, thus have the lowest insurance premium.

As a commercial property owner, you want to know the construction type of your building so you can understand how it affects your coverage options and costs. You also want to understand how the type affects your lessor’s risk insurance. That way, you can work toward a balance of coverage and cost that fits your situation.

How to Reduce Your Lessor’s Risk Insurance Premium

A lessor’s risk insurance premium isn’t fixed. You can lower it by improving your property’s safety features. Some of the features that can help you save money on your premium are:

- Sprinkler system: This is a system that automatically sprays water in case of fire. It can prevent or reduce fire damage to your property. It can also lower your fire risk rating and your insurance premium. But it can also increase your replacement cost, because you have to replace the sprinkler system if it’s damaged. You have to weigh the pros and cons of having a sprinkler system.

- Fire alarm: This is a system that alerts you and the fire department in case of fire. It can help you respond quickly and minimize fire damage to your property. It can also lower your fire risk rating and your insurance premium. It doesn’t increase your replacement cost as much as a sprinkler system.

- Burglar alarm: This is a system that alerts you and the police in case of burglary. It can help you address theft or vandalism exposure on your property. It can also lower your theft risk rating and your insurance premium. It doesn't increase your replacement cost.

As a commercial property owner, you want to invest in your property's safety features. Making your property more secure and less risky will both help safeguard it and lower your lessor's risk insurance premium.

How to Get a Credit for Occupying Your Own Property

Lessor’s risk insurance is not only for properties that you rent out entirely. It’s also for properties you occupy partially. If you have a property with multiple units or bays you can run your own business in one of them. Then rent out the rest to other businesses.

You may have the same name for your business and property and want to insure both under the same policy. You can do that with lessor's risk insurance. It can cover your property and your business.

It also covers the property you lease to others. But there’s a benefit to occupying your own property. You may get a credit on your insurance premium.

A credit is a discount or a reduction. Employing this method may allow you to pay less for your insurance. This is because you have more control and supervision over your property. You can prevent or fix problems faster and reduce the risk of damage or liability.

You can also improve the safety and quality of your property. As a commercial property owner and occupant, look into getting a credit for occupying your own property. Ask your agent or insurance carrier about this option. Doing so might help you save money and help address your property and business coverage needs at the same time.

How to Help Protect Yourself as a Lessor with a Triple Net Lease

A triple net lease is a lease structure where the tenant pays for everything. They pay for the rent, the taxes, the insurance, and the maintenance. They’re responsible for the building as if they own it, so they have to insure the building.

This may sound good for you as a lessor. You don't have to pay for or worry about anything. But you still have to be careful and take steps to look after your interests. That means making sure the tenant has a valid and adequate insurance policy.

Beyond that, request to be included in the policy as an additional insured and a certificate holder. You want updated information about the policy as they happen, such as being notified if or when the policy lapses or gets canceled. You have to make sure that the tenant can pay for any damage or liability that may occur.

If you don’t do these things, you may be in trouble. You may lose your property or your income and face legal issues or claims. You may not be able to rebuild or restore your property or find another tenant. You don’t want to take these chances by failing to obtain a lessor’s risk insurance policy.

A lessor's risk policy can provide an important layer of coverage for your property and help address liability exposure that may arise from your tenant's insurance situation. It may provide added composure as a commercial property owner.

Lessor's Risk Insurance: What CNY Property Owners Should Know

Commercial property ownership in Central New York comes with real exposure — from tenant-related liability to vacant property gaps to construction-type factors that affect your premium. Ignoring lessor's risk insurance, or carrying an inadequate policy, can leave you with costs and legal exposure you weren't prepared for.

In this article, we covered how lessor's risk insurance works, why vacant properties still need coverage, how tenant selection affects your insurability, and steps you can take to help manage your premium.

At the Horan insurance agency, we work with several carriers to help CNY commercial property owners explore lessor's risk coverage options that fit their situation and their budget. We're not here to make promises about outcomes — we're here to help you understand your options.

Click the Get a Quote button below to connect with one of our licensed agents and start the conversation about lessor's risk coverage for your property.

{kind=link}