You run a landscaping business in Central New York, and you don't want to make an uninformed insurance decision. Between managing crews, maintaining equipment, and keeping clients satisfied through unpredictable CNY weather, you worry that you might purchase a policy that isn't quite right for your situation—or worse, discover a gap in coverage after something goes wrong on a job site.

At the Horan insurance agency, we understand this concern. As an independent agency working with multiple carriers, we can provide an informed perspective to help you explore coverage options designed for landscaping operations. We work with landscaping companies throughout the CNY region and can help you understand the types of policies available to address your specific risks.

In this article, we'll walk through the common types of landscaping insurance, explain what each one covers, and show you how to begin evaluating options for your business.

What to Consider When Choosing Landscaping Insurance

Not all landscaping insurance policies are the same. Depending on the services you offer and the size of your business, you may need different types of coverage to suit your needs.

For example, if you only do lawn care, you may need different coverage than if you also do hardscapes or tree trimming. And if you have employees or use vehicles for your work, you may need additional coverage as well.

Here are some of the common types of landscaping insurance that may benefit your business:

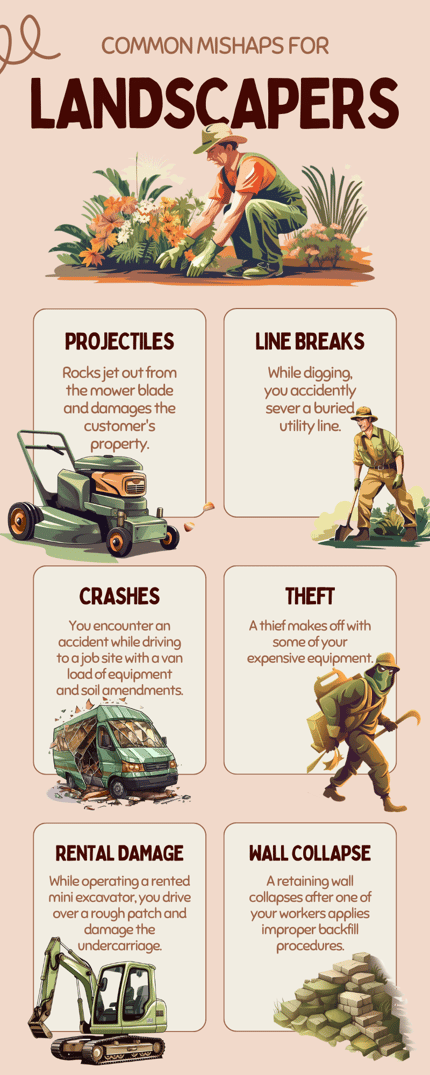

General Liability Insurance

Let’s look at property damage and bodily injury coverage in more detail.

- Property Damage. Suppose you’re transforming a client’s backyard into a beautiful oasis, but an accident happens, and your crew accidentally damages a valuable water feature or ornamental fixture. The costs of repairing or replacing the damaged property can quickly add up, potentially leading to disputes and financial stress.

- Bodily Injury. As you work hard to create amazing outdoor spaces, there’s always a risk of someone getting injured on the job site. Perhaps a client or a passerby accidentally trips over an exposed cable, resulting in a painful fall and subsequent medical expenses. This can lead to legal claims, leaving you vulnerable to costly lawsuits.

Commercial Property Insurance

As a landscaper, you likely own equipment, tools, and supplies that are essential for your work. Commercial property insurance can help cover your business property, including your office, tools, machinery, and other assets, from risks such as fire, theft, vandalism, or natural disasters.

As a landscaper, you likely own equipment, tools, and supplies that are essential for your work. Commercial property insurance can help cover your business property, including your office, tools, machinery, and other assets, from risks such as fire, theft, vandalism, or natural disasters.

To put that into perspective, a couple of examples include:

- Equipment Theft. Your tools and machinery are vital to your landscaping business. Sadly, thieves are always on the lookout for valuable equipment and may target yours. If your equipment gets stolen, not only could you face the monetary loss of replacing it, but your business operations may also be disrupted until you can acquire new tools.

- Natural Disasters. Nature can be awe-inspiring but also destructive. Imagine a severe and characteristic CNY storm ripping through the area, causing significant damage to your office, storage facilities, or even your equipment. The aftermath of such events can be emotionally draining and financially overwhelming.

Commercial Auto Insurance

If you use vehicles for your landscaping business, such as trucks, vans, or trailers, you’ll need commercial auto insurance. It provides coverage for accidents, property damage, and injuries caused by your vehicles while they’re being used for business purposes.

As a landscaper, you rely on your vehicles to transport equipment and travel between job sites. However, even the most careful drivers can be involved in accidents. Whether it’s a collision with another vehicle or damage caused by hitting a pothole, a single accident can result in substantial repair costs for your vehicle and potential liability for injuries sustained by others involved.

If you don’t have commercial auto insurance for your landscaping vehicles, you could expose your business to serious financial and legal risks. A personal auto policy typically won’t cover your vehicles if they’re involved in an accident while being used for business purposes.

You could face hefty fines, lawsuits, and liability claims that could jeopardize your business assets and reputation. To help address these risks, you should consider switching to a commercial auto policy as soon as possible.

To learn more about when and how to make the switch, check out our article “When Should Small Contractors Switch from Personal to Commercial Auto Insurance?”

Workers Compensation Insurance

If you have employees, workers compensation insurance is generally mandatory in New York State. It provides coverage for medical expenses, lost wages, and rehabilitation costs if an employee is injured on the job. It can help address concerns for both you and your employees in case of work-related injuries or illnesses.

Your employees work hard to help you bring clients’ landscapes to life. However, the physical nature of the job can put them at risk of injuries. From slips and falls to muscle strains or even serious accidents involving machinery, any work-related injury can result in medical expenses and potential lawsuits.

Having workers compensation insurance in place can provide crucial support to your employees and may help reduce your business's exposure to liability. Read more about the benefits of workers comp coverage.

Professional Liability Insurance

Also known as errors and omissions insurance, professional liability insurance is crucial for landscapers who provide design or consulting services. It covers you against claims of negligence, errors, or omissions that may result in financial losses or damage to a client’s property.

In the case of Errors in Design or Consultation, let’s say you’re a landscaper who offers design or consultation services.

You may face claims from clients who are unhappy with the results or feel you made mistakes that cost them money or harmed their property.

Say you suggest a plant that turns out to be invasive or unsuitable for the client’s climate. Professional liability insurance can help cover the costs of defending yourself against such claims and paying any settlements or judgments that may arise.

Business Interruption Insurance

This coverage helps protect your business income if you experience a significant disruption that prevents you from working, such as a natural disaster or a fire at your office. It can help cover your ongoing expenses and lost income during the period of interruption.

But let’s see it at work.

Suppose strong lines of thunderstorms roll into the area and damage your office and storage facilities, rendering them unusable for several weeks. During this time, you may lose income from canceled or postponed projects, as well as incur expenses for repairs and temporary relocation.

Business interruption insurance can help reimburse you for these losses and expenses until you can resume your normal operations.

Inland Marine Insurance

If you transport your equipment or tools to different job sites, inland marine insurance can provide coverage for your property while it’s in transit. It may help address loss or damage to equipment during transportation, including theft, accidents, or vandalism.

We’ll look at an example that involves Equipment Damage.

Imagine you’re transporting your equipment and tools to a new job site in Radisson, but along the way, your trailer gets into an accident and flips over. The impact damages or destroys some of your valuable equipment and tools, leaving you with a hefty repair or replacement bill.

Inland marine insurance can help cover the cost of repairing or replacing your damaged or lost equipment and tools.

Explore Coverage Options for Your Landscaping Business

As a CNY landscaper, you face risks that are specific to your line of work—from equipment damage and vehicle accidents to on-the-job injuries and liability claims. The right combination of coverage can make the difference between a manageable setback and a serious financial disruption.

But sorting through policy options on your own can be confusing and time-consuming. You may not be sure which types of coverage apply to your operation or whether your current policy leaves gaps that could expose you to unnecessary risk.

That's where we come in. As an independent agency, we work with multiple carriers and can help you compare options side by side. We can walk you through the details, answer your questions, and help you make informed decisions about coverage for your landscaping business.

Click the Get a Quote button below to start exploring your options. One of our licensed insurance agents will follow up with you.

Topics:

{kind=link}