You did the responsible thing and bought car insurance, so you assume the drivers around you in CNY did the same. The trouble is, many didn't, and a quiet portion of the cars sharing I-690, Route 481, and the village streets of Baldwinsville carry no coverage at all, or carry so little that one serious crash could leave you with bills the other driver can't cover.

That gap is unsettling, especially when you've done everything right. A minimum-limits policy gives you a foothold, but it may not go far if you're seriously injured by someone with no coverage or thin coverage of their own. You shouldn't have to learn that the hard way after a crash.

At the Horan insurance agency in Baldwinsville, we work with many carriers across CNY, which gives us a clearer view of how uninsured and underinsured motorist coverage fits into a New York auto policy. We can help you compare options so the choice fits your situation rather than a generic template.

In this article, we'll walk through how uninsured and underinsured motorist coverage works in New York, why the state minimum often falls short, how supplementary coverage fills the gap, and what these coverages do — and don't — pay for.

What is Uninsured and Underinsured Motorist Coverage?

Uninsured and underinsured motorist coverage is insurance coverage you buy from your auto insurance carrier to cover your medical bills if you're hit by a driver who doesn't have any car insurance or has insurance coverage that is too low to cover your expenses. But uninsured motorist and underinsured motorist coverage work differently, as you'll see below.

Uninsured and underinsured motorist coverage is insurance coverage you buy from your auto insurance carrier to cover your medical bills if you're hit by a driver who doesn't have any car insurance or has insurance coverage that is too low to cover your expenses. But uninsured motorist and underinsured motorist coverage work differently, as you'll see below.

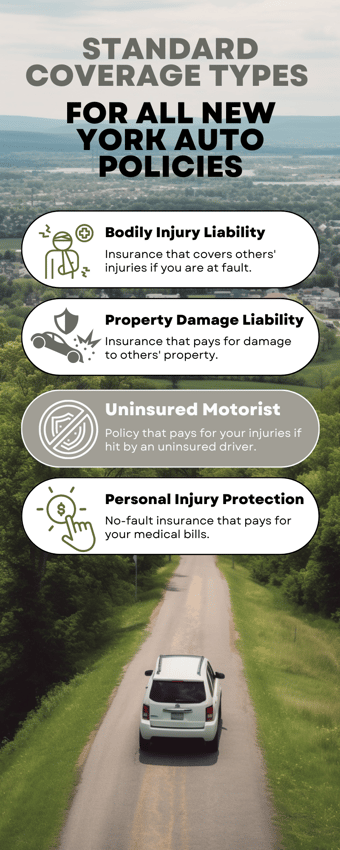

- Uninsured motorist coverage covers you in case of an accident with a driver who has no insurance or whose insurance company denies or cannot pay their claim.

- Underinsured motorist coverage covers you in case of an accident with a driver who has some but not enough insurance to cover all of your injuries.

The Danger of Uninsured Drivers

Driving without insurance is a serious problem in the United States. According to a March 2021 report by the Insurance Research Council (IRC), nearly 13% of drivers (meaning one out of every eight drivers in the United States) had no car insurance in 2019.

The IRC’s data showed that the percentage of uninsured drivers has increased steadily since 2010, and it is likely that the number of uninsured drivers has continued to increase since 2019. This means that there are millions of drivers on the road who are not financially responsible for any damage or injuries they may cause in an accident.

IRC found that uninsured drivers are more likely to be involved in accidents (including fatal ones) and cause more damage and injuries than insured drivers. There are three reasons for this:

- They’re likely to drive more recklessly. Drivers who don’t have insurance may be more likely to drive recklessly because they don’t have to worry about the financial consequences of an accident. They may be more likely to speed, drive under the influence of alcohol or drugs, or engage in other risky behaviors.

- They tend to shirk the rules of the road. Drivers without insurance may be less likely to obey the rules of the road because they don’t have to worry about getting a ticket. They are also more likely to run red lights, speed, or tailgate.

- Their vehicles are often in poor working order. These drivers are also less likely to have their cars in good working order because they don’t have to worry about the cost of repairs. They often drive cars with bald tires, faulty brakes, or other mechanical problems.

This is why it's important to have suitable uninsured and underinsured motorist coverage against uninsured drivers. This coverage can help cover you financially if you're involved in an accident, regardless of whether the other driver is insured.

The Mandatory New York State Minimum for Uninsured and Underinsured Motorist Coverage

In New York State, car insurance policies come standard with some coverage against uninsured drivers. However, the minimum requirement is identical to the state's bodily injury liability limits, meaning that the most you would have available if severely injured by an uninsured driver is $25,000.

If other passengers in your vehicle were also hurt, the maximum available would be $50,000, with no one person exceeding a $25,000 payment.

It's important to note that if you were in an accident with an insured driver visiting from Pennsylvania, where the minimum insurance requirement is only $15,000, underinsured motorist coverage can fill the gap between the other driver's bodily injury limit and your underinsured limit.

Since uninsured and underinsured limits are combined and share the same coverage amount, you’d have $10,000 available in this scenario.

Supplementary Uninsured and Underinsured Coverage Options

As mentioned in our comprehensive auto insurance article, you have options beyond the low $25,000 limit for uninsured and underinsured motorist coverage. One option is to add supplementary uninsured and underinsured motorist coverage.

Supplementary coverage works in the same way as its uninsured motorist counterpart, but it gives you the option to build upon the low $25,000 limit per injured person.

With supplementary coverage, you can purchase as much coverage as your carrier will allow, with one stipulation: your supplementary limits cannot be higher than your bodily injury liability limits. For example, if you carry $250,000 per person bodily injury coverage, you can purchase up to that amount in supplementary coverage.

While it's possible to buy less supplementary coverage compared to your bodily injury limits, you must sign a form indicating your intention to do so. But we don't recommend this as the added cost of supplementary coverage is negligible compared to the rest of the policy.

Will Uninsured or Supplementary Coverage Cover Damages to My Vehicle?

So far, we've been discussing injuries to you as a person, but what about damage to your car caused by an uninsured driver? In New York, your uninsured or supplementary coverage will not cover this. Your only option would be to file a claim using your policy's collision coverage.

Without collision coverage on your auto policy, there would be no coverage provided by your insurance. Even if you have collision coverage, you would still be responsible for paying your collision deductible.

Is Uninsured and Supplementary Coverage the Same as "No-Fault" Coverage?

Neither uninsured nor supplementary coverage is the same as no-fault or Personal Injury Protection insurance. They have their differences.

- No-fault or Personal Injury Protection coverage is designed to help cover you financially if you're injured in an accident, regardless of who is at fault.

- Uninsured and supplementary coverage is designed to help cover you financially if an uninsured or underinsured driver causes an accident that injures you.

While these coverages provide coverage for similar claims, uninsured and supplementary coverage are considered secondary to your Personal Injury Protection insurance coverage and are generally not used until your Personal Injury Protection insurance has been depleted.

In New York, Personal Injury Protection provides a mandatory $50,000 in coverage for both you and your passengers. Any injury expenses come from your policy first, regardless of the other driver's insurance status. To learn more about how this coverage works, read our article "What is New York No-Fault Insurance?"

Increase or Supplement Uninsured Coverage for Stronger Backup

With a possible rise in uninsured and underinsured drivers on the road whose reckless behavior remains unchecked, being struck by one of these drivers is a real danger.

Uninsured motorist coverage helps cover your long-term pain and suffering and medical bills if you're hit by one of these drivers. But the base $25,000/$50,000 limit won't be enough to cover you after an accident that leads to substantial injuries.

You deserve better backup.

Supplementary uninsured and underinsured motorist coverage is available with higher limits, as we've stated, often up to the amount of the policy's bodily injury limits. It provides broader coverage for bodily injury you may suffer.

We can help you review your policy and discuss whether raising your uninsured coverage or adding supplementary coverage may be suitable for your situation. You should contact your agent to do so.

Drive CNY Roads With More Than the Minimum Behind You

We covered how uninsured and underinsured motorist coverage works in New York, why the $25,000 state minimum often falls short, how supplementary coverage can build on that base, and how this coverage sits alongside no-fault.

With a clearer view of these pieces, you can talk through your auto policy with more confidence — and avoid the surprise of finding out, after a crash, that the limits you carried weren't enough.

Leaving the decision for "someday" is the part that tends to hurt later. A reckless driver doesn't check your policy before pulling into your lane on Route 31 in Baldwinsville or merging onto I-481 near Cicero. The right time to look at your limits is before any of that happens.

As an independent CNY agency, the Horan insurance agency works with many carriers, which gives us a vantage point a single-carrier office doesn't have. We'd like to be a steady resource for you as you weigh your auto coverage.

Click the Get a Quote button below to start a conversation about your uninsured and underinsured motorist limits.

Topics:

{kind=link}