As a Central New York retail owner, you pour your heart and soul into creating a thriving business. But unexpected events like fires, injuries, or lawsuits can threaten your dreams. At Horan Insurance, we understand.

We specialize in crafting tailored insurance solutions that shield your unique retail venture from the unexpected.

In this article, we'll navigate the insurance maze so you can have the right coverage for:

- Customer mishaps: in case someone gets hurt in your store and sues you.

- Building disasters: for when your brick-and-mortar haven encounters a devastating storm, fire, or other covered peril.

- Inventory woes: adaptive policy protection to cover your supply during seasonal fluctuations.

- Employee concerns: keeps your team covered if work injuries happen or family leave is required.

Read on to learn more about the types of insurance you need as a Central New York retail owner.

Defining a Retail Business in CNY

Retail companies sell products directly to consumers from a physical storefront. Goods may range from food items to clothing, furniture, automotive parts, and beyond. If that description fits you, read on.

As a retail business owner in Central New York, you face various risks and challenges every day. You may encounter customer injuries, property damage, theft, vandalism, fire, or weather-related disasters. You may also face lawsuits from employees, customers, or competitors.

These events can disrupt your operations, damage your reputation, and cost you a lot of money.

That’s why you need retail insurance to protect your business from the unexpected. Retail insurance is a type of business insurance that covers the specific needs and risks of retail businesses like yours. It can help you pay for medical expenses, legal fees, property repairs, lost income, and more in case of a covered claim.

Basic Insurance Needs for Most CNY Retail Outlets

The type and amount of retail insurance you need may vary depending on your business size, location, industry, and inventory. However, most retail businesses in CNY should have at least the following coverages:

- General liability insurance: This covers your legal liability if someone gets injured or their property gets damaged because of your business activities. For example, if a customer slips and falls on your wet floor, general liability insurance can help pay for their medical bills and your legal defense.

- Commercial property insurance: This covers your physical assets, such as your building, equipment, furniture, inventory, and signage, from damage or loss caused by fire, theft, vandalism, or weather. For example, if a storm damages your roof and some of your inventory, commercial property insurance can help pay for the repairs and replacements.

- Business interruption insurance: This covers your lost income and extra expenses if you have to temporarily close or relocate your business due to a covered property loss. For example, if a fire forces you to shut down your store for a month, business income insurance can help cover your lost sales and rent for a temporary location.

These three coverages are often bundled together in a business owner’s policy (BOP) or a commercial package policy (CPP). Both can save you money and simplify your insurance process. A BOP or CPP is a convenient and affordable way to get the essential protection you need for your retail business.

Accurately Value Your Business Property and Inventory for Retail Insurance

With retail insurance, you want to accurately value your business property and inventory. This includes not only the items that are essential for running your business, such as furniture, point of sale systems, and computer equipment, but also the items that you sell or store, such as inventory, shelving, and display cases.

These items can represent a significant investment and a major source of income for your business. If they’re damaged or destroyed by a covered event, such as a fire, storm, or burglary, you want to make sure that you have enough coverage to replace them at their current market value.

Therefore, you should regularly update your inventory records and appraise your business property to reflect their true worth. This will help you avoid underinsuring or overinsuring your assets and paying more or less than you should in premiums and deductibles.

Properly Insure Your Retail Store Building and Its Improvements

Owning a business comes with a variety of responsibilities, one of which is protecting your physical space and the valuable assets within it. But what happens when your property extends beyond the basic walls and roof? This is where the concept of business personal property insurance and tenant improvements comes into play.

Owning the Building

If you own your business premises, know that your standard homeowner’s insurance won’t extend coverage. You’ll need a commercial property insurance policy specifically designed to cover the building itself, its contents, and any potential liabilities.

Renting the Space

Even as a renter, you have valuable property to safeguard. This includes any permanent improvements or alterations you’ve made to the space, such as upgraded flooring, custom built-in shelves, or specialized lighting. These additions, while enhancing your business, are often not covered by your landlord’s insurance.

That’s where business personal property (BPP) insurance steps in.

BPP: Your Safety Net for Tenant Improvements

BPP insurance acts as a safety net, protecting your financial investment in those improvements you’ve made to the rental space. Whether it’s a fire, theft, or unexpected damage, having BPP ensures you won’t be left footing the bill for replacing these valuable assets.

A Common Business Property Oversight

Unfortunately, many business owners overlook the importance of including tenant improvements in their BPP coverage. This can leave them exposed to significant financial losses if something unforeseen occurs. Remember, BPP is not just for furniture and equipment; it’s for the entirety of your business’s tangible property.

By understanding the distinction between building coverage and tenant improvement protection, you can ensure your business is fully shielded. Don’t settle for a policy that leaves gaps in your coverage. Talk to your insurance agent to discuss your specific needs and get a BPP policy that reflects the true value of your investment.

Consider Peak Season Coverage

As a retail shop owner in Central New York, you know that your business can vary based on the season. Maybe you sell more during the holidays or the summer months, depending on what kind of products you offer. For example, if you sell swimming pool supplies, you probably have more inventory in the warmer months than in the winter.

But what if a fire breaks out in your store when you have more stock than usual? You could lose a lot of valuable merchandise that is flammable or explosive, such as toys, equipment, and chlorine. That’s why you need peak season coverage on your business owners policy.

Peak season coverage is a special feature that automatically increases your inventory coverage during certain times of the year, when you expect to have more goods on hand than normal. You don’t have to call your insurance carrier and ask for a temporary increase in your coverage limit. You just need to specify the percentage of increase and the months when it applies.

For instance, if you normally have $100,000 worth of inventory, but you have 50 percent more during June, July, August, and September, you can get peak season coverage that will raise your limit to $150,000 for those four months. This way, you can rest assured that you’re adequately protected in case of a fire or other disaster.

Peak season coverage is especially important for businesses that sell seasonal items, such as florists, gift shops, clothing stores, and so on. If you have a lot of inventory for Valentine’s Day, Mother’s Day, or other special occasions, you want to make sure that you have enough coverage to replace it if something goes wrong.

Peak season coverage is one of the essential components of a comprehensive business owners policy for retail shops. It’s a smart way to protect your inventory and your profits from seasonal fluctuations.

Employee Insurance for Retail Businesses

As a retail business owner with employees in Central New York, you’re required to protect your workers in case they get hurt or sick because of their work. This includes workers compensation insurance. Workers comp covers your employees’ medical expenses and lost wages if they have a work-related injury or illness.

You can also choose to cover yourself as the owner, or not. This is a common decision for retail business owners. If you don’t cover yourself, you save money on the insurance premium. But you also give up the right to receive benefits if you suffer a work-related injury or illness.

You have to consider the risks and benefits of this option. If you do cover yourself, you pay more for the insurance premium. But you also get the security of the policy if you need it. However, the amount of coverage is not based on your actual income. It’s based on a minimum income set by the insurance company.

This minimum income varies by occupation. For example, if you’re a retail store manager and an owner, the insurance company may assume you earn $50,000 a year. This is the basis for your workers compensation coverage.

And if you have employees, you have to provide them with New York State short term disability and paid family leave. Workers compensation regulates them and ensures you have them in place.

Customizing Your Business Insurance with Endorsements

A business owners policy can also include endorsements that suit your specific type of retail business. Endorsements are modifications or additions to your policy that cover certain risks or exposures. For example, you may need cyber liability insurance or product liability insurance.

These endorsements vary by the carrier and the occupation. Cyber liability insurance protects your business from claims of data breaches, hacking, or identity theft. This is important if you store sensitive customer information or conduct online transactions.

Product liability insurance protects your business from claims of bodily injury or property damage caused by your products. This is important if you sell or distribute goods that could potentially harm your customers or third parties.

You need to check with your carrier and your agent to see what endorsements are available for your business owners policy.

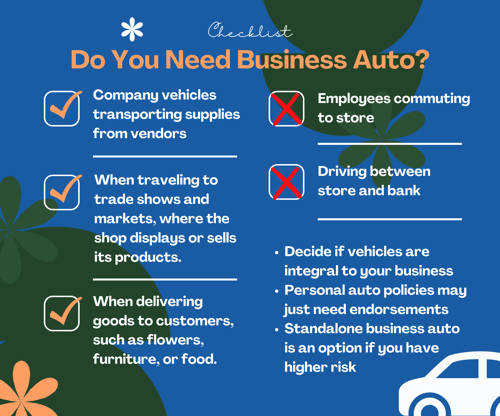

Commercial Auto Insurance

Another thing to consider is how you use your vehicle for your retail business. If you offer delivery services, for example, you need a policy that covers the business use of your vehicle. You can either add an endorsement to your personal policy to include business use, or you can get a separate commercial auto policy.

This depends on how your business operates and how you use your vehicles. Do you or your employees use cars to deliver goods to customers or suppliers? If so, existing personal vehicle policies need business endorsements.

Alternatively, you can opt for a separate commercial auto policy. This is different from a business where driving is not essential for your work, but only for commuting or personal tasks. Many people fall into this category and don’t rely on their car for their business.

However, if you do, you need to secure yourself and your business from any legal or financial consequences in the event of a crash. A commercial auto policy is the answer.

Buy Business Coverage That Keeps Your Retail Shop Properly Shielded

Running a retail business requires grit, passion, and vigilance. But protecting your dream shouldn’t feel like another challenge. With the right insurance plan, you can trade worry for focus, knowing your investments, team, and future are shielded.

Imagine facing a storm-damaged storefront with composure. Picture weathering a customer injury lawsuit with security. Visualize peak seasons flowing seamlessly, knowing your fluctuating inventory is protected.

The cost of overlooking crucial coverage can be far greater than the cost of proactive protection.

Don’t let the unexpected derail your retail journey. Get a personalized consultation from us. We can build a tailored insurance plan that empowers you to breathe easy, sell strong, and achieve your retail dreams.

Click the Get a Quote button below to get started. Our insurance specialists are ready to help.

Topics:

{kind=link}