You love your car, but you know that it’s not getting any younger. Every year, it loses some of its value due to wear and tear, mileage, and market conditions. This can be a problem if you ever get into an accident and your car is totaled—which happens when the cost of repairing the car exceeds its value.

You might end up owing more on your loan than what your insurance company will pay you for your vehicle. How can you avoid this situation and help shield yourself from losing money on your car?

We understand that having a totaled car can be a stressful and frustrating experience. You may feel angry, sad, or helpless about losing your car and having to pay for a new one. You may also worry about how to cover the gap between your loan and your insurance payout.

Knowing what to do next or who to turn to for help doesn't come easy in moments like this. That's why we're here to support and guide you toward a favorable outcome for your situation.

As a Baldwinsville agency, we've been writing auto policies for CNY residents for years, working to fit coverage to their vehicles and loans. We've used our knowledge and experience to help them find a suitable option for their vehicles and loans. And we've compiled this info to help do the same for you.

In this article, we’ll explain what it means to have a totaled car, how insurance companies determine the actual cash value of your car, and what options you have to cover the gap between your loan and your car’s worth.

After reading to the end, you’ll be in a better position to take wise action with your auto policy and reduce the risk to your financial stability.

How Your Car’s Value and Repair Cost Determine If It’s Totaled

How Your Car’s Value and Repair Cost Determine If It’s Totaled

What does it mean to have a “totaled” car? You might think that it means your car is so badly damaged that it can’t be driven or repaired. But actually, it can take very little to total a car. It all depends on how much your car is worth and how much it would cost to fix.

When you have comprehensive and/or collision insurance on your car, you're insuring it for its actual cash value (ACV). This is the maximum amount of money your insurance company will pay you if your car is totaled.

ACV is based on the current market value of your car, not the price you paid for it when it was new. That’s why

even minor damage, such as a broken tail light or a cracked bumper, can total your car if the repair cost exceeds its value.

But let’s make it even clearer.

Suppose your car is worth $3,000. You’re flying along Leland Avenue in North Utica and hit a pothole, hard. The engine mounts, which hold the engine in place and absorb vibrations, crack due to the impact. The engine takes excessive damage, along with other parts, and the car is leaking fluids.

Fixing it will run you $3,800, $800 more than the vehicle is worth.

That means your carrier will declare your car totaled and pay you its ACV, minus your deductible. If your deductible is $500, you’ll receive $2,500. The insurer will then keep your car for salvage.

If you don’t have a loan on your car, this process can be fairly simple. But what if you do?

Let’s say you still owe $2,900 on your loan. Since your car is the collateral for the loan, the bank will get the $2,500 check from the insurance company. You’ll have to pay the remaining $400 out of pocket.

The insurance company is not responsible for covering the difference between your loan and your car’s value.

This situation can be worse for newer cars, which lose considerable value as soon as they leave the dealership. That’s why some people buy GAP insurance, which covers the gap between the ACV and the loan balance.

GAP insurance is usually included in the loan and is typically available only for new or almost-new cars. GAP insurance would likely not apply to the previous example.

Factors That Affect Your Car’s Actual Cash Value and When to Dispute It

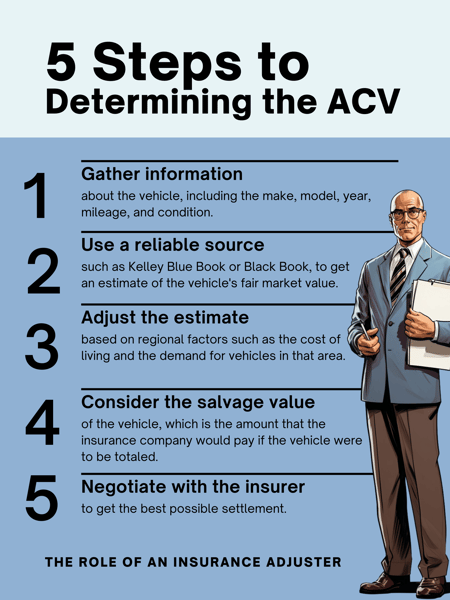

When an insurance company’s adjuster determines the actual cash value (ACV) of your car, they use several sources of information. They start with services like Kelley Blue Book or Black Book, which give general estimates based on the make, model, year, and condition of the car.

Then they adjust these estimates according to regional factors, such as the impact of salt on the roads in the CNY area. Finally, they consider the salvage value of the car, which is how much they can earn by selling its parts at an auction. After this research, the adjuster will present you with their value calculation.

You have the right to challenge this calculation if you think it is unfair. You may be able to get more compensation if you can provide evidence that your car is worth more than what they offer.

If you choose to keep your car after it’s declared a total loss, you should know that the insurer will reduce the money they pay you.

This is because they’ll deduct the salvage value from the ACV since they won’t be able to sell your car’s parts. You should also be aware that you won’t be able to buy comprehensive or collision coverage for your car anymore.

You’ll have to pay for any future repairs out of pocket.

Don't Let a Totaled Car Strain Your Finances

If you have a car loan, you may be at risk of losing money if your car is totaled in an accident. This is because your car’s value may have depreciated faster than your loan balance, creating a gap that your insurance company won’t cover. This can leave you with debt and no car to drive.

This is the situation you'll face if you overlook the points we've made here. You need to understand how insurance companies calculate the actual cash value of your car, and what options you have to help guard against the gap.

By following our tips, you’ll be able to make informed decisions about your car and your loan and save yourself from unnecessary financial stress.

By reading this article, you’re already demonstrating responsibility and care for your vehicle.

A totaled car is a common and unpredictable situation that can affect anyone. So you should be aware of the factors that affect your car’s value and insurance coverage.

But if you’re not sure about your vehicle’s value or how it affects your current policy in relation to your loan, we can help. We certainly don’t want you to experience the financial burden a total loss can create.

We can compare different quotes and coverages from various insurers and explain the pros and cons of each. We can also advise you on how to get GAP insurance, which can cover the difference between your loan and your car’s value in case of a total loss.

Getting things started is as easy as clicking the Get a Quote button below. Once you supply a few details for us, one of our friendly agents will reach out to you to discuss your auto policy options.

Rather continue the auto insurance learning journey? Read “Comprehensive vs. Collision Insurance: What’s the Difference?”

Topics:

{kind=link}