Hitting the open road on a motorcycle in Central New York offers a unique sense of freedom. But before you twist the throttle, it’s crucial to understand how motorcycle insurance differs from car insurance. While both require minimum liability coverage, the specific risks and coverage options for motorcycles create a distinct path.

At the Horan insurance agency, we understand the thrill of riding a motorcycle in Central New York. We’re also keenly aware of the unique insurance needs that come with this exhilarating experience.

Since 2009, our team of dedicated agents has used their deep understanding of local risks and regulations to tailor policies that fit the specific riding style and budget of CNY riders.

This article will navigate you through the key differences between motorcycle and car insurance, helping you choose the right policy for your two-wheeled adventures.

We’ll explore essential coverages like medical payments and accessory protection, along with how factors like riding frequency and safety courses impact your insurance rates.

With that, let’s dive into the world of motorcycle insurance in Central New York.

Understanding Your Coverage: Motorcycle vs. Car Insurance

When you’re looking to hit the road in New York, whether you’re revving up your motorcycle or buckling up in your car, the state’s liability requirements remain consistent. You’ll need minimum coverage of

- $25,000 for bodily injury per person,

- $50,000 for total bodily injury, and

- $10,000 for property damage

This is commonly referred to as 25/50/10 coverage.

That’s the baseline for legally taking your vehicle out for a spin. But once you’ve met these minimums, the similarities between motorcycle and car insurance start to veer off.

Here’s where they diverge:

Liability insurance may operate under the same principles across motorcycles and cars, but the risks involved with each ride are distinct. Motorcyclists face a different set of hazards on the road, which is reflected in the structure of their insurance policies.

From the cost of premiums to the details of accident coverage, understanding these differences is key to choosing the right policy for your journey.

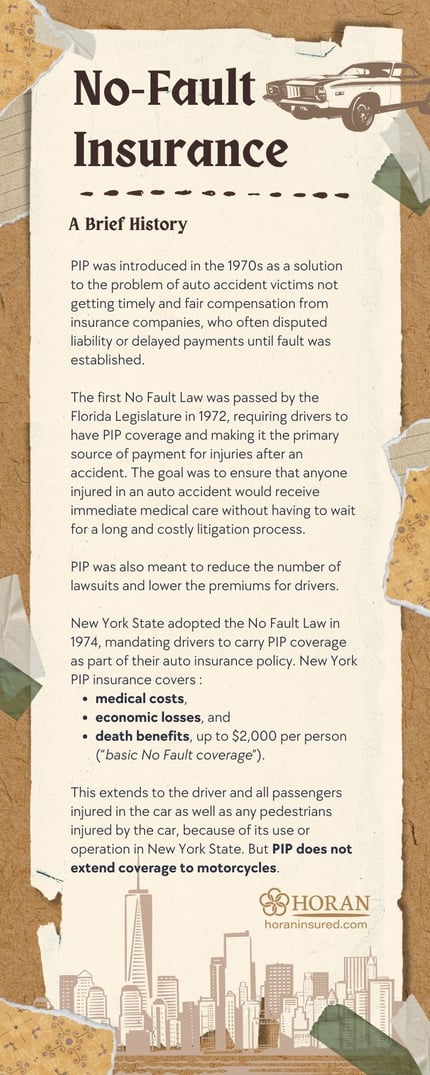

Navigating Personal Injury Protection: A Split Road for Motorcyclists and Drivers

Diving into the heart of insurance disparities, we find personal injury protection (PIP) at the forefront. Here’s the twist: while car drivers are cushioned by PIP in the event of an accident, motorcyclists find themselves without this safety net.

Diving into the heart of insurance disparities, we find personal injury protection (PIP) at the forefront. Here’s the twist: while car drivers are cushioned by PIP in the event of an accident, motorcyclists find themselves without this safety net.

The reason? The inherent risks of motorcycling.

Back when PIP was being shaped in the ’70s, lawmakers recognized the stark contrast in potential injuries between car accidents and motorcycle crashes. Covering motorcyclists under PIP could mean consistently maxing out benefits due to the severity of injuries sustained.

After all, when a motorcyclist is involved in a high-speed accident, the likelihood of life-threatening injuries or extensive medical needs is high—often surpassing the PIP limits.

In contrast, car occupants typically experience less severe injuries in crashes, leading to shorter recovery periods and less medical expenditure. This disparity is why PIP coverage for motorcyclists wasn’t deemed feasible.

Instead, medical payments coverage steps in to address the gap, offering motorcyclists a tailored solution for their unique road risks. Understanding this key difference is crucial when selecting the insurance that best fits your two-wheeled lifestyle.

Maximizing Medical Payments Coverage: A Key Strategy for Motorcyclists

In the realm of auto insurance, medical payments coverage often takes a backseat due to PIP’s role in covering medical expenses. Typically, this coverage ranges from $1,000 to $10,000, and it’s there for those rare instances when PIP isn’t applicable—like if you’re at fault in a DUI incident.

However, for motorcyclists, this coverage takes on a pivotal role. Without the cushion of PIP, it’s wise to amp up your medical payments coverage to the highest amount possible. Progressive Insurance, for instance, offers up to $25,000.

Securing this level of coverage can provide significant financial relief in the event of an accident, as it directly pays for your medical expenses, much like PIP would, up to the covered amount.

While it won’t cover lost wages or other expenses, it’s a crucial piece of protection for every rider. It’s the financial safety gear you hope you’ll never need but will appreciate having if the unexpected happens.

So, when you’re choosing your motorcycle policy, remember: investing in robust medical payments coverage isn’t just smart—it’s essential.

Accessorizing Your Ride: The Importance of Coverage for Motorcycle Add-Ons

When it comes to motorcycles, the personal touch means everything. Riders often enhance their bikes with various accessories, from practical saddlebags to flashy chrome extensions, not to mention high-tech upgrades like custom stereos. These personalizations don’t just add style. They add value to your ride—and potential risk.

When it comes to motorcycles, the personal touch means everything. Riders often enhance their bikes with various accessories, from practical saddlebags to flashy chrome extensions, not to mention high-tech upgrades like custom stereos. These personalizations don’t just add style. They add value to your ride—and potential risk.

Here’s where accessory coverage becomes crucial for motorcycle insurance. Unlike car insurance, which doesn’t prioritize accessory coverage, motorcycle insurance policies often provide options to protect these valuable add-ons.

Whether it’s custom parts or aftermarket enhancements, ensuring they’re covered is as important as insuring the bike itself.

So, if you’re decking out your bike, remember to talk to your insurer about extending your coverage to include all those personal investments. It’s not just about safeguarding against theft or damage. It’s about preserving the unique character of your motorcycle that makes it truly yours.

The Frequency Factor: How Usage Influences Motorcycle Insurance Rates

Motorcycle insurance takes a different road when it comes to determining rates. Unlike car insurance, which often considers your daily commute and overall vehicle usage, motorcycle insurance policies zoom in on how often you ride.

Since many use their motorcycles for leisure rather than daily transportation—especially in Central New York climates not conducive to year-round riding—this frequency of use significantly impacts your premium.

Typically, motorcycles are insured under separate policies, tailored to the unique risks and usage patterns of riders. However, some carriers like Erie Insurance offer the convenience of bundling motorcycle coverage with auto policies.

But more often than not, riders turn to specialists like Progressive or Geico, who offer policies crafted specifically for the needs of motorcyclists.

When it comes to the value of your bike, insurance companies handle it much like they do cars. If your motorcycle is damaged beyond repair, they’ll assess its actual cash value, accounting for depreciation, to determine the payout.

So, while the approach to premiums may differ, the fundamental principles of valuation remain consistent across both types of vehicles.

The Incentives of Experience and Safety Courses in Motorcycle Insurance

Motorcycle insurance offers unique incentives that are not found in car insurance policies. One such incentive is the discount for completing a motorcycle safety course. This educational benefit is exclusive to the world of two-wheelers and can lead to savings on your insurance premiums.

Experience also plays a more pronounced role in motorcycle insurance. While car insurance may not heavily weigh your years of driving past a certain age, motorcycle insurers often consider your riding experience.

The more seasoned you are in the saddle, the better your chances of securing a competitive rate—or even qualifying for a policy at all.

Affordable Motorcycle Insurance: Riders Save More Than Car Owners

When it comes to cost, motorcycle insurance generally carries a lighter price tag than its four-wheeled counterpart.

For instance, you might secure a liability-only policy for an older motorcycle for around $100 a year—a figure that’s virtually unheard of in car insurance. On average, motorcycle policies tend to range between $300 and $400 annually, though the exact cost can vary based on coverage levels and other factors.

It’s a nuanced equation, but one that often tips in favor of the motorcycle owner.

Fuel Your Journey with Confidence by Getting Tailored Motorcycle Insurance

Central New York’s open roads beckon, but a smooth ride requires preparation. We covered the key distinctions between motorcycle and car insurance, empowering you to make informed decisions.

While skimping on coverage might seem like a way to save money upfront, a single accident can wipe out those savings and leave you financially vulnerable. The right insurance policy acts as a shield, deflecting unexpected blows and giving you composure and security as you navigate the twists and turns of the road.

Horan is here to help you. We’ll guide you through the intricacies of motorcycle insurance, ensuring you have the coverage you deserve for a worry-free ride.

Click the Get a Quote button below for a free consultation and quote and let’s get you back on the open road with confidence.

Topics:

{kind=link}