Owning a barbershop is your dream. You pour your heart into every cut, building a loyal clientele and a thriving business. But what if a customer gets injured on your watch, even though they weren't seeing you directly? The legal and financial fallout could shutter your doors.

At Horan Insurance, we understand the unique challenges Central New York barbershop owners face. We've seen countless dreams threatened by unforeseen accidents, and we're here to help you avoid that nightmare.

This article unveils a simple but often overlooked insurance strategy that protects your business and composure. It's not just about chairs and scissors; it's about safeguarding your passion and the future you've built.

Ready to discover the secret weapon for barbershop security? Keep reading.

Which of These Two Ways Do You Run Your Barbershop?

If you own a barbershop, you need to protect your business from various risks. Depending on how you operate your barbershop, you may need different types of insurance. There are two common ways to run a barbershop:

- You are the proprietor, and you hire employees to cut hair for you.

- You rent out chairs to independent contractors who cut hair under your establishment.

In this article, we will cover both scenarios and help you find the best insurance for your barbershop in Central New York. If you rent out chairs and don’t have employees, you can skip to that section. If you have employees, read on to learn more.

Insurance for a CNY Barber with Employees

If you’re a barbershop owner with employees, there are a few key types of insurance coverage you should consider:

- General Liability Insurance: This protects against claims of bodily injury or property damage that might happen in your barbershop.

- Business Property/Contents Coverage: This covers damage to or theft of your business property, not just things like razors, combs, and brushes, but also more expensive items like barber chairs, sinks, vanities, and plumbing.

- Workers compensation insurance: This covers your employees’ medical expenses and lost wages if they get injured or sick on the job. For example, if one of your employees slips and falls on a wet floor while carrying scissors, this insurance will pay for their hospital bills and missed workdays. Learn more about workers comp coverage.

- Short-term disability insurance: This provides partial income replacement for your employees if they are unable to work due to a non-work-related injury or illness. For example, if one of your employees breaks their arm while playing soccer on the weekend, this insurance will help them cover their living expenses until they can return to work. If you have employees, New York State requires you to carry Workers Comp and Disability Insurance. Learn more about short-term disability.

The core package to look into is a Business Owners Policy (BOP). This bundles together property, liability, and other common small business insurance needs into one policy.

Make sure to work with an agent who understands the unique risks barbershops face. They can help you evaluate potential gaps and ensure adequate protection for your business.

Barber and Beautician Professional Liability Insurance

This coverage is different from general liability insurance, or a BOP, which only covers bodily injury or property damage. Barber and beautician insurance covers other types of harm, such as:

- Emotional distress: Let’s say you accidentally botch a groom’s haircut just before his weekend wedding at Belhurst Castle on the shores of Seneca Lake. He endures emotional stress because of this and decides to sue you. This coverage helps pay for the legal fees.

- Financial loss: Say you use a product that causes an allergic reaction or a chemical burn to your customer’s scalp, this insurance will cover the medical costs and any lawsuits that may arise.

- Reputational damage: Suppose you give your customer a bad haircut and they post a negative review online. They may sue you for harming their reputation. Barber and beautician professional liability insurance is also critical in this instance.

Most insurance companies that offer business coverage for barbershops also offer this endorsement for professional liability. It’s not very expensive, so it’s worth it. It will protect you from lawsuits and claims that could otherwise cost you a lot of money and harm your local brand.

You can read our related article for an even deeper dive on how professional liability coverage works.

This insurance applies to both barber scenarios, whether you have employees or not. However, if you have employees, you should have a BOP. You also need workers compensation and short-term disability insurance, as we explained before.

Chair Rental Insurance: Vital Protection for Your Barbershop

Owning a barbershop that rents out chairs offers a unique business model, generating income from your own services and those of independent barbers.

While these independent barbers are responsible for having their own liability insurance, often called “chair rental insurance,” simply requiring it isn’t enough for complete security.

What Type of Insurance Does a Chair Renter Need?

While a “chair rental” policy exists, it often makes more sense for independent barbers to opt for a Business Owners Policy (BOP). This comprehensive policy typically bundles general liability, property, and other essential coverages if necessary.

The specific coverage limits and types needed will vary depending on your business activities and risk profile. We recommend you consult with your insurance agent to tailor the coverage to your specific situation.

Why Chair Rental Insurance Matters

Imagine a scenario where a customer suffers an allergic reaction to a product used by an independent barber in your shop. Even though the barber carries their own insurance, the customer might still associate the incident with your business, potentially harming your reputation and leading to legal action.

As the owner, you have the responsibility of ensuring that your business is adequately protected. This is where additional steps become crucial.

Building a Safety Net

Building a Safety Net

Here are two key actions you can take to safeguard your barbershop if you rent chairs to independent barbers:

- Require Additional Insured Status: Ensure each barber’s chair rental insurance policy lists you as an “additional insured.” This means you’ll receive direct notifications of any policy changes, lapses, or cancellations, allowing you to take proactive measures if necessary. No more relying on barbers to remember and inform you.

- Minimum Coverage Standards: Implement a minimum coverage requirement for all barbers renting chairs. Consider at least $500,000 in liability coverage, with $1 million being even better. While the cost increase might seem minimal, the added protection is invaluable.

- Implement Annual Verification: Request updated insurance certificates from each barber annually. This simple step confirms they maintain active coverage, providing you with ongoing composure.

The Benefits of Proactive Protection

Investing in these measures offers several advantages:

- Reduced Stress and Risk: Knowing you have additional safeguards in place minimizes the stress and financial burden associated with unforeseen incidents.

- Prompt Action and Awareness: Timely notifications of policy changes enable you to address any issues swiftly, potentially preventing escalation or complications.

- Safeguarding Your Reputation: By ensuring proper insurance coverage for all service providers within your shop, you minimize the risk of your business reputation being negatively impacted by incidents involving independent barbers.

Chair rental insurance, even with professional liability and high coverage limits, is typically quite affordable. Requiring it will result in the long-term security of your business.

Regardless of who rents the chair, customers associate your name and brand with the services offered within your shop. Making sure comprehensive coverage is carried by everyone operating in your space is vital.

By taking these proactive steps and requiring chair rental insurance with “additional insured” status and annual verification, you can build a robust safety net for your barbershop. This not only protects your business financially but also helps maintain your hard-earned reputation within the community.

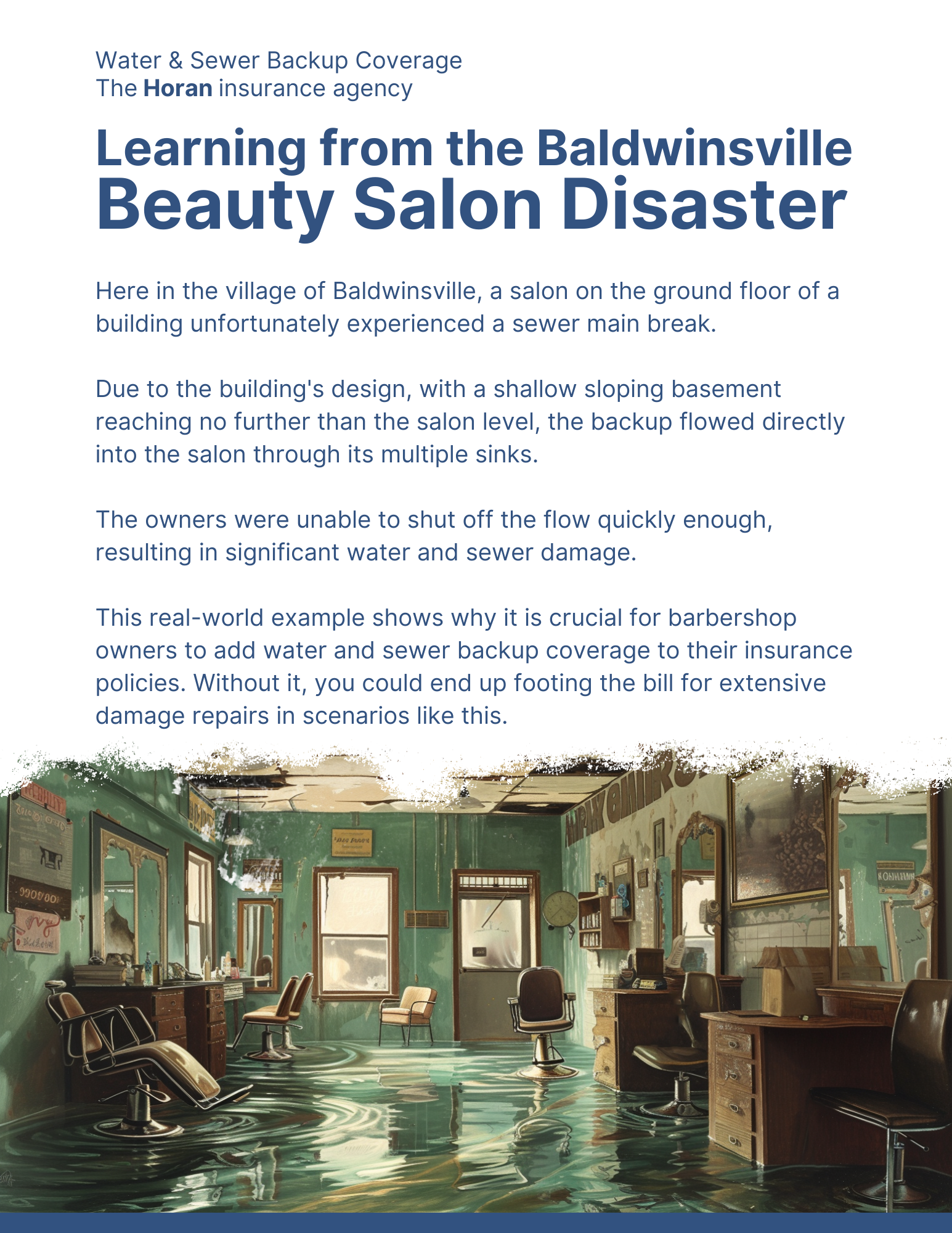

Protect Your Business from Sewer and Water Backups

This is especially crucial for businesses like barbershops and beauty salons with plumbing fixtures, especially those that regularly wash hair. While not all barbershops offer hair washing, those that do are particularly vulnerable.

Sewer and water backup damage can be extensive and costly, impacting everything from furniture and equipment to inventory and even building structure.

Considerations for Water and Sewer Backup Coverage

- Assess your risk: Evaluate the potential for backups based on your location, building plumbing, and past incidents.

- Choose appropriate coverage: Discuss your needs with your insurance agent to ensure sufficient coverage for potential damage.

- Regular maintenance: Preventative maintenance on your plumbing system can help reduce the risk of backups.

By taking these steps, you can ensure you’re protected from the financial burden of sewer and water backup events.

Learn more about protecting your business from water and sewer backup disasters.

Get the Business Policy That’s Right for Your Barbershop

The final snip of the day shouldn’t be the sound of a lawsuit closing your doors. Your focus should be on the intricate details of a client’s desired style, not the legalese of a liability claim. That’s the transformative power of proper barbershop insurance.

Overlooking this crucial protection might seem like a harmless gamble, but the potential losses are far from a friendly wager. A single, unforeseen incident involving an independent barber or client mishap could clip the wings of your barbershop dream, leaving you entangled in legal battles and financial burdens.

Don’t let a preventable mishap snip away the future you’ve meticulously built.

If you follow the advice in this article, you’ll have the right insurance for your barbershop. Safeguards from various risks and liabilities will be in place for you, your staff, your customers, and your property. You’ll have composure and security for your business. And you’ll be able to focus on what you do best: cutting hair and making people happy.

We’ll work with you to craft a customized insurance plan that shields your business from unforeseen storms, so you can create a haven for happy clients and a thriving business that buzzes with success.

Click the Get a Quote button below to start protecting your barbershop business with the right coverage.

Topics:

{kind=link}